The HDB MOP or Minimum Occupation Period requires you to occupy your flat for a set period before you can consider selling your flat. Regarding HDB MOP rules, the MOP is usually five years for most HDB homebuyers, but there are other considerations.

HDB MOP rules apply regardless of circumstances or even if you can purchase a much more expensive property. Maybe you have a couple of kids now, and a 3-room HDB flat is too small. Or you need to move closer to your ageing parents.

Whatever your considerations, we want to help you better understand how to buy your next home. If you are already familiar with the HDB MOP rules and ready to start selling your home, let us help.

Video on HDB MOP Rules in Singapore

Unfamiliar with HDB MOP rules? Watch this quick video to understand what they are.

1. When Does My Minimum Occupation Period End?

| Flat bought from HDB and HDB resale flat bought on the open market | Five years (for Plus and Prime flats, it is 10 years) |

| DBSS flat | Five years |

| SERS flat | For SERS sites announced on/after 7 April 2022, five years from collecting your keys For SERS sites announced before 7 April 2022, seven years from the date of selecting your replacement flat or five years from collecting your keys, whichever is earlier |

| Fresh Start Housing Scheme HDB flat | 20 years |

The first question probably have is when exactly your HDB MOP ends. For resale flat MOP, the answer is pretty straightforward. It’s from when your flat purchase is legally completed.

This may be unclear because even within the same BTO project, households collect their keys in different phases and move in at different times. To answer, for those with BTO flats, your MOP end date is five years from when you collect your keys to the HDB flat. So according to HDB MOP rules, if you were one of the earliest to move in, congrats! You’re one step ahead.

But if you have a Prime BTO flat launched under the Prime Location Public Housing (PLH) model – or a Plus BTO flat in the future, your MOP is 10 years.

If you don’t want to sieve through documents when you collect your keys or calculate how long it’s been, you can simply log in to the My HDBPage website. On My HDBPage, you can find your resale flat MOP date or BTO flat MOP date.

If you’re interested in buying a freshly MOP-ed HDB resale flat, here’s a list we’ve compiled for you. Otherwise, when browsing PropertyGuru listings, you can use the search and filter function to sort available projects by neighbourhoods, build year, pricing range, and more.

Browse HDB REsale Flat Listings

Looking for a freshly MOP-ed HDB flat?

Are There Any HDB MOP Exemptions?

If you want to appeal to HDB to waive your MOP, you should have a valid reason. Whether for a new flat or resale flat MOP waiver, the decision for MOP exemptions is subject to HDB’s discretion and is assessed on a case-by-case basis.

Reasons for cases that were approved include “financial hardship, divorce, or the demise of the owner”. If you have clear evidence, there is a good chance HDB will seriously consider your case. If not, HDB MOP rules should be followed, and we do not advise you to try to bend them!

2. Can I Apply for BTO Before My MOP Is Fulfilled? Can I Apply for a Second BTO Flat or EC If the Completion Date Is after My MOP?

You might be wondering: since a new BTO or Executive Condominium (EC) would take years to complete, can you apply for a new home before the MOP is up? What about if the completion date of the new BTO flats or EC is after your MOP?

Unfortunately, the answer to "Can I apply for BTO before MOP" is no. You can only apply for your second BTO HDB flat or EC after you have fulfilled your MOP for your current HDB flat. No earlier, no exceptions.

That means you probably won’t be able to move right after the five-year mark unless you buy a completed or resale property. If you’re eyeing a new BTO flat or EC, the timeline is likely to be like this:

- Five years in the first BTO

- Apply for a second BTO or new EC

- Continue living in your first BTO until the new property is ready

- Move to the new property

- Sell your existing flat

3. Can I Buy a Private Property Before Selling My HDB Flat?

Yes, however, there will be certain ramifications to the loan limit and cash outlay for your private property purchase.

Firstly, if you have an outstanding loan for your HDB flat, then your maximum borrowing limit for the private property will be limited to 45% of its value rather than 75%.

This equates to a much higher cash outlay for your down payment. Since there’ll be a period between when you have two housing loans (after you buy the new property, but before you sell the old one), you’d also have to ensure you fall within the Total Debt Servicing Ratio (TDSR), where the amount of monthly loan repayments you have to make is less than 55% of your gross monthly income.

The second issue is the potential Additional Buyer’s Stamp Duty (ABSD) incurred. Let’s say you’re looking to buy an investment property. Since this is your second property and you’re a Singapore citizen, you will incur a 20% ABSD.

But if you intend to sell your HDB flat and live in the private property, you would be eligible for a remission of the ABSD amount if you sell the first property within six months. However, you will still have to cough up the cash for the ABSD tax first.

4. How Much Money Do I Need to Refund Into My CPF OA?

When you want to upgrade to a bigger home, you typically need to pay a larger downpayment as it will be more expensive. This is when you may start calculating whether you would have enough cash for the down payment and renovation costs after refunding your CPF.

In general, you must refund any funds used for your purchase. This may include the initial downpayment, administrative fees and stamp duty, monthly mortgage repayments, government housing grants, and accrued interest on all funds used. This may significantly deplete the amount of cash you think you’d get in hand.

Do not worry, though, as you will probably be able to use the bulk of your refunds for your next property purchase. The only concern would be how much cash in hand you’d get to retain.

5. Must I Pay HDB Resale Levy When Upgrading to a Private Property?

If you are selling your current subsidised flat to purchase another one directly from HDB or an EC, you are required to pay the HDB resale levy.

HDB Resale Levy Amount

2-room flat

$15,000

$7,500

3-room flat

$30,000

$15,000

4-room flat

$40,000

$20,000

5-room flat

$45,000

$22,500

Executive flat

$50,000

$25,000

EC

$55,000

Not applicable

However, if upgrading to a resale HDB flat or private property, you don’t have to fork out any HDB resale levy. And as always, before you upgrade your property, plan your budget carefully. You want to factor in all these upfront costs, have extra just in case an unexpected expense occurs, and ensure you are not too financially stretched.

6. What Is the Timeline for the Sale of HDB Flat?

For most people, you would look to sell your HDB flat first before upgrading to a private property as this means you don’t have to pay any ABSD taxes, you can use the sales profits for your next downpayment, and you will still qualify for the higher loan limit (first mortgage).

In such a scenario, the following outlines the steps required to complete the sale of your HDB home and to buy your private property.

Selling the HDB Flat

- Register Intent to Sell and find an interested buyer

- Buyer signs Option-To-Purchase (OTP)

- Buyer exercises OTP

- Seller and buyer submit HDB resale application

- HDB accepts the application

- The sale is completed, and the handover begins

Buying the Private Property

- Find preferred private property to buy

- Buyer sign OTP

- Buyer exercises OTP

- The sale is completed, and the handover begins

The exact timeline of selling your HDB flat to buying and moving into your private property is hard to specify. But typically, it takes anywhere from two to six months. It could be longer if you cannot find a buyer or preferred home or if there are administrative delays.

Prefer a real-life example? Read about how one of our writers sold her freshly MOP-ed BTO flat to buy a resale condo and what she learned from the experience.

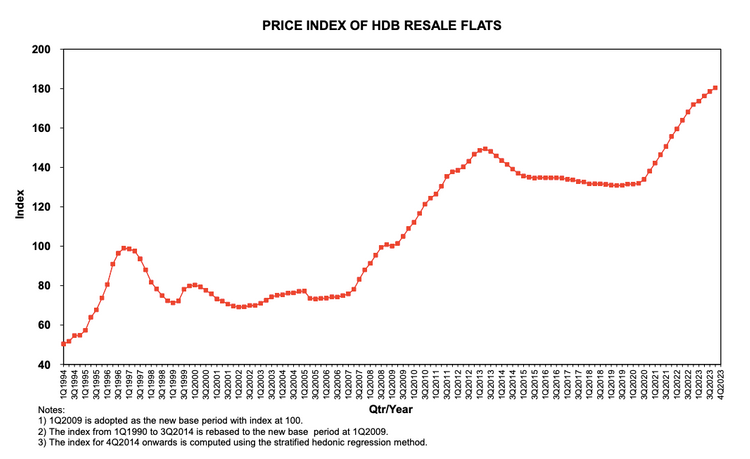

7. How Much Can I Get for My HDB Flat and How Much Are Other Resale HDB Flats?

To know whether you are getting a good price for your flat, you must know where the property cycle is. HDB resale flat prices dipped and held relatively steady after reaching a high in 2013.

However, the COVID-19 pandemic saw many construction delays, which pushed many buyers into the resale market. In turn, prices for HDB resale flats soared and are now at an all-time high. However according to the Singapore Property Market Outlook 2024, signs of price resistance have been spotted, and price growth has slowed significantly.

If you intend to sell your first home, you can likely turn a tidy profit, especially if it is a BTO flat. For those who have fulfilled your resale flat MOP and are selling, you could make some profit if you had bought your home at an opportune time.

To understand what property price transactions are in your vicinity, you can search for similar HDB resale flat listings on PropertyGuru. After clicking into a listing, you can scroll down to the ‘Pricing Insights’ section, where you’ll see recent price trends and transaction details.

You can also explore the filters in our. From these figures, you can make a good ‘guesstimate’ on how much to sell your current property for and how much to offer for a new one. Alternatively, use our property valuation tool.

8. Is Now a Good Time to Upgrade to a Bigger Flat or Private Property?

Many people aspire to upgrade, but most simply stay on the sidelines wondering when to bite the bullet as property prices climb higher and higher beyond their reach.

You may have noticed that HDB and private property prices in Singapore tend to rise. Over the years, what’s considered the ‘new low’ is likely to be still higher than the previous low. Likewise, the ‘new high’ is expected to be higher than the previous high. Following this logic, wouldn’t every time be a good time to buy?

As you can see, it’s hard for anyone to tell you the best time. So instead of trying to time the market, we encourage you to assess your finances and work out your priorities before deciding.

Currently, resale flat prices are at an all-time high, as are private property prices. If you sell high now, there’s a good chance you’re also buying high, so you may need to calculate your options carefully.

For those who intend to buy an HDB flat, apply for your HDB Flat Eligibility (HFE) letter. At the stage where you’re doing a preliminary HFE check, you will get information on your housing eligibility and financing options, including how much grant amount you are eligible for. This information will help with flat budget planning for your next home.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.