In Singapore’s real estate landscape, the Additional Buyer’s Stamp Duty (ABSD), a supplementary tax added on top of the standard Buyer’s Stamp Duty (BSD). Whether you are a first-time homebuyer or a property investor, it is important to understand what is absd singapore, when ABSD applies, how much it costs, and when you may qualify for reliefs or remissions.

When you buy a residential property, you must pay BSD. Depending on your residency status, number of properties owned, or if the purchase is made through an entity or trust, you may also need to pay ABSD.

The ABSD for 2nd property is generally higher than for the first one, reflecting Singapore’s efforts to moderate investment demand. The rates were last revised on 27 April 2023 as part of the property cooling measures and remain in effect in 2025.

Under the current structure:

- The ABSD for foreigners buying any residential property was raised from 30% to 60%.

- Singapore citizens and permanent residents (PRs) also pay higher ABSD rates on their second and subsequent properties.

- In March 2025, the government announced further updates to the ABSD regime for licensed housing developers, allowing more flexibility for complex projects.

There is also relief for senior Singapore citizens who sell a higher-value private home and rightsize to a smaller one. They may qualify for an ABSD refund under specific conditions.

Looking for a smoother property search?

Save your preferences on our app and get listings tailored to you.

Watch Our Video on Additional Buyer’s Stamp Duty (ABSD) in Singapore

What Is Additional Buyer’s Stamp Duty (ABSD) in Singapore?

Additional Buyer’s Stamp Duty (ABSD) is a tax imposed on certain residential property purchases in Singapore, charged in addition to the standard Buyer’s Stamp Duty (BSD), based on the buyer’s residency status and the number of properties they own.

ABSD Table (2025): What Are the Current Additional Buyer’s Stamp Duty Rates in Singapore?

Understanding the latest ABSD rates helps you estimate your total property cost more accurately. The ABSD table below shows the updated Additional Buyer’s Stamp Duty (ABSD) rates in Singapore for 2025.

Singapore Citizens (SC)

0%

20%

30%

Permanent Residents (PR)

5%

30%

35%

Foreigners

60%

60%

60%

Entities / Trusts (non-individuals)

65%

65%

65%

Housing Developers (for residential property)

35% (plus 5% non-remittable)

35% (plus 5% non-remittable)

35% (plus 5% non-remittable)

The ABSD Singaporean rate varies depending on the number of properties owned, while Singapore citizens enjoy lower rates for their first and second homes; higher duties apply from the third property onwards.

Thinking of buying a home?

Find out how much you can afford before you start your property hunt.

Note: These rates are based on IRAS’s schedule for ABSD on residential property as of 27 April 2023 and remain in force.

How Are ABSD Rates Calculated?

ABSD is calculated based on the purchase price or the market value of the property, whichever is higher.

The applicable rate depends on the buyer’s profile (Singapore Citizen, Permanent Resident, Foreigner, or Entity) and the number of residential properties already owned at the time of purchase.

For example, if a Singapore Permanent Resident buys a second residential property priced at $1,000,000, the ABSD rate of 30% applies.

So, PR ABSD = $1,000,000 × 30% = $300,000

The ABSD amount must be paid within 14 days from the date of the sale and purchase agreement (if executed in Singapore) or 30 days if executed overseas.

Stamp Duty Calculator

Estimate your property stamp duty in seconds.

ABSD Definition of ‘Residential Property’ in Singapore

Under Singapore’s ABSD rules, a residential property refers to properties intended primarily for dwelling purposes. It includes most housing types but excludes commercial, industrial, and certain land types.

Types of Residential Property:

HDB Flats

New or resale flats built by HDB

ABSD may not apply to first-time SC buyers

Executive Condominiums (EC)

Hybrid of public and private housing

Treated as private property after 10 years for resale

Private Condominiums / Apartments

High-rise residential buildings

ABSD applies based on the buyer profile and the property count

Landed Properties

Terraced, semi-detached, detached houses

Higher ABSD rates for second or subsequent properties

Note:

- Residential property does not include commercial buildings, offices, industrial units, or land not zoned for housing.

- ABSD is calculated based on purchase price or market value, whichever is higher.

ABSD Definition of ‘Entity’ in Singapore

An entity refers to non-individual buyers acquiring residential property. ABSD rules apply differently to entities, often with higher rates than those applied to individual buyers.

Examples of Entities:

| Type of Entity | ABSD Implication |

| Companies | ABSD rate of 65% for any residential property |

| Trusts | Treated as entities; ABSD at 65% |

| Partnerships / Associations | Also subject to 65% ABSD |

Notes:

- Entities may be eligible for limited ABSD remission under strict conditions.

- Entities acquiring property for development or resale may face additional ABSD obligations.

ABSD Exemptions in Singapore

Specific buyers can be fully or partially exempt from ABSD under particular conditions.

First-time SC Buyer

Singapore Citizens purchasing their first property

0% ABSD

Government / Statutory Bodies

Property bought for public purposes

No ABSD payable

Inheritance / Court Orders

Property transferred due to inheritance or divorce

ABSD is exempt if conditions are met

Downsizing Seniors

Senior SC is selling a higher-value property and buying a smaller one

Eligible for remission/refund

Key Points:

- ABSD exemptions require proof of eligibility and may involve an application to IRAS.

- Certain reliefs are time-bound; for example, applications must be submitted within a set period after purchase.

ABSD Remission for Foreigners Married to Singaporeans

Foreigners buying property with a Singapore Citizen spouse may qualify for partial or full ABSD remission, depending on the circumstances.

Eligibility Criteria:

| Condition | Requirement |

| Joint Purchase | Property must be jointly bought with the SC spouse |

| Residential Property | Must be the primary home for the couple |

| Remission Application | Submit to IRAS within 14 days of S&P execution (Singapore) or 30 days if overseas |

Key Points:

- ABSD remission reduces the ABSD payable by the foreign spouse’s share.

- Only residential properties are eligible.

- Couples must document marital status and joint ownership for IRAS verification.

Who Needs to Pay ABSD in Singapore?

Additional Buyer’s Stamp Duty (ABSD) is a supplementary tax on top of the standard Buyer’s Stamp Duty (BSD), aimed at regulating residential property ownership in Singapore. Whether you are required to pay ABSD depends on your residency status, the number of properties you already own, and, in some instances, whether the purchase is made through an entity or trust. Understanding who needs to pay ABSD is critical before committing to a property purchase.

Singapore Citizens (SC)

- First property: ABSD does not apply, which encourages homeownership for first-time buyers.

- Second property: ABSD applies at 20% of the property’s purchase price or market value, whichever is higher.

- Third and subsequent properties: ABSD increases to 30%, reflecting government measures to moderate speculative property investment.

- Example: If a Singapore Citizen buys a second property valued at $1,000,000, the ABSD would be $200,000 (20% of $1,000,000).

Permanent Residents (PRs)

- First property: ABSD is 5%, slightly higher than SCs to manage demand.

- Second property: ABSD is 30%.

- Third and subsequent properties: ABSD is 35%.

- PRs should carefully consider property purchases, as ABSD can significantly increase overall costs.

Foreigners

- Any residential property purchased by a foreigner is subject to a flat 60% ABSD, regardless of whether it is the first property.

- Example: A foreign buyer purchasing a $1,000,000 condominium will pay $600,000 in ABSD.

- This measure is designed to moderate foreign investment demand and maintain affordability for local buyers.

Entities / Trusts (Non-Individuals)

- Companies, partnerships, associations, and trusts acquiring residential properties are subject to 65% ABSD.

- Entities purchasing property for development or resale may have additional obligations.

- Certain exemptions or reliefs may be available under strict conditions, but they are limited.

Licensed Housing Developers

- For developers buying residential sites for construction, ABSD is 35% plus 5% non-remittable, reflecting government controls on the supply of new properties.

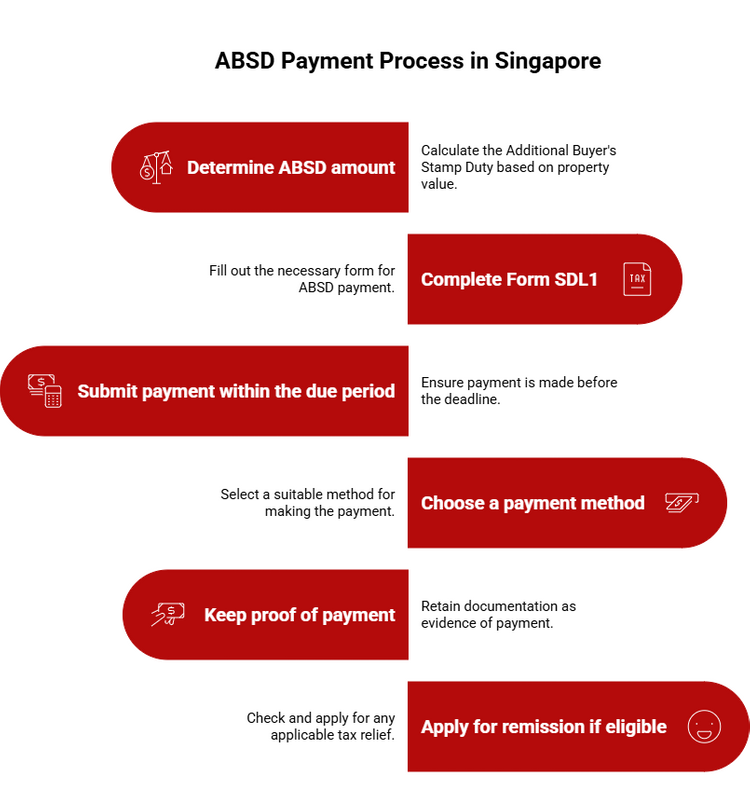

How to Pay ABSD in Singapore?

Follow these steps to pay ABSD correctly and on time:

- Determine ABSD amount

- Calculate ABSD based on the higher of the purchase price or the market value of the property.

- Check the applicable ABSD rate for your buyer profile (SC, PR, Foreigner, or Entity).

- Calculate ABSD based on the higher of the purchase price or the market value of the property.

- Complete Form SDL1

- Use the IRAS e-Stamping portal to fill in the ABSD form.

- Ensure all buyer details and property information are accurate.

- Use the IRAS e-Stamping portal to fill in the ABSD form.

- Submit payment within the due period.

- 14 days from signing the Sale & Purchase Agreement (S&P) if in Singapore.

- 30 days if the S&P is executed overseas.

- 14 days from signing the Sale & Purchase Agreement (S&P) if in Singapore.

- Choose a payment method.

- Online via IRAS e-Payment or GIRO.

- At IRAS counters, you can use cash, cheque, or card.

- Online via IRAS e-Payment or GIRO.

- Keep proof of payment.

- Retain receipts or e-payment confirmation for records and future verification.

- Retain receipts or e-payment confirmation for records and future verification.

- Apply for remission if eligible.

- For certain buyers, such as seniors downsizing or foreigners married to Singaporeans, it is recommended to submit ABSD remission applications before making the payment.

Worried about paying extra ABSD?

Learn smart, legal ways to cut down your property tax costs.

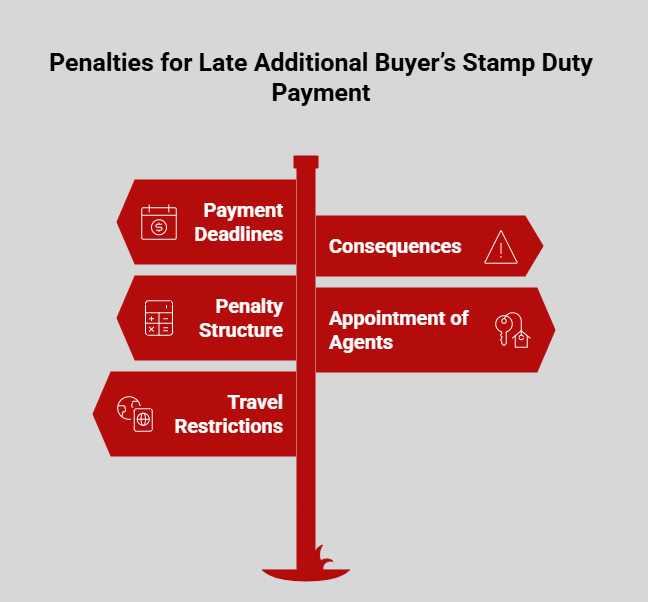

Are There Any Penalties for Late Payment of Additional Buyer’s Stamp Duty?

Paying ABSD on time is mandatory. Failure to do so can result in penalties, enforcement actions, and travel restrictions.

1. Payment Deadlines

- Within 14 days after signing the Sale & Purchase Agreement (S&P) if executed in Singapore.

- Within 30 days after receiving the document in Singapore, if the S&P is signed overseas.

Note: For electronic documents, they are considered received in Singapore if:

- Accessed or retrieved by a person in Singapore.

- Stored on a device brought into Singapore.

- Stored on a computer located in Singapore.

2. Consequences for Late Payment or Non-Payment

IRAS may take the following actions:

- Impose penalties based on the duration of the delay.

- Appoint agents such as your bank, employer, tenant, or lawyer to recover the unpaid ABSD.

- Issue a Travel Restriction Order (TRO) preventing you from leaving Singapore.

- Take legal action (including fines or property seizure).

Note: ABSD must be paid even if an objection is filed and under review. Any overpayment due to revised assessments will be refunded.

3. Penalty Structure

| Delay Duration | Penalty |

| Up to 3 months | $10 or an amount equal to ABSD due, whichever is greater |

| Over 3 months | $25 or 4 times ABSD due, whichever is greater |

| Voluntary Disclosure | 5% of late payment or underpayment per year, calculated daily (if disclosed under IRAS’ Voluntary Disclosure Programme) |

4. Appointment of Agents

- IRAS can appoint banks, tenants, lawyers, or other third parties to recover unpaid ABSD.

- If your bank is appointed, you may face restrictions on accessing your account until payment is completed.

- Agent release occurs only after full payment of ABSD and penalties.

5. Travel Restrictions

- A TRO prevents leaving Singapore until ABSD and penalties are fully paid.

- A Notification for the Release of the TRO is sent within 10 days after payment, allowing exit at immigration checkpoints.

- Non-NRIC holders must ensure a valid pass to remain in Singapore while resolving ABSD matters with IRAS. Overstaying is an offence.

Should You Try to Avoid Additional Buyer’s Stamp Duty?

The Additional Buyer’s Stamp Duty (ABSD) is a legal tax imposed on certain property purchases in Singapore based on your residency status and the number of properties you own.

The 2nd property stamp duty under ABSD is higher than for a first home, which often prompts buyers to explore ways to manage the cost. However, attempting to avoid ABSD through illegal means can lead to hefty penalties, legal action, and even travel restrictions.

Instead, buyers should focus on legal ways to manage ABSD. They can plan property purchases to qualify for first-property exemptions or jointly buy with an eligible Singapore Citizen spouse for partial remission.

ABSD relief schemes are also available when downsizing or meeting other qualifying conditions. Paying ABSD on time and using the available legal remissions and exemptions remains the safest and most compliant approach.

For more property news, content, and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.