Executive Condominiums (ECs) remain a popular housing option in Singapore, offering a blend of public and private living.

As of 2025, the EC market remains active, with several projects launched and more in the pipeline. For instance, in 2024, the Lumina Grand EC saw 53% of its units sold at launch, indicating strong demand. The Housing & Development Board (HDB) has released sites for future EC developments, such as the one opposite Downtown East in Pasir Ris, signalling continued interest in this housing type.

In this updated guide for 2025, we will explore the latest developments in the EC market, executive condo eligibility criteria, available CPF housing grants, and the procedures for purchasing an EC. Whether you’re a first-time buyer or considering upgrading, this guide will provide you with the information needed to navigate the EC landscape effectively.

Find Your Ideal Home Faster

Stop browsing endlessly. Save your search on our app and get personalised property listings that match your needs.

Watch Our Video on Buying Executive Condos in Singapore

Executive Condominium Market Overview: 2025 Key Insights

In 2025, Executive Condominiums (ECs) are expected to remain a popular and affordable entry point into private housing in Singapore. The EC market has seen significant activity in new launches and resale transactions, reflecting both strong demand and healthy price appreciation trends underpinned by HDB upgraders transitioning into ECs or private housing.

Key highlights on 2025 ECs in Singapore are summarised in the table below:

| Category | Details |

| Number of new EC units launched (1H 2025 GLS) | 980 units |

| Price range for new EC launches (per sq ft) | S$1,300 to S$1,700 PSF |

| EC units transacting over $1 million (resale, 2H 2024) | 38 units |

| Average resale price premium: new launch condos vs resale condos (2025) | 47% premium; $2,618 PSF vs $1,781 PSF |

| Average sales price in the Outside Central Region (OCR) for new launches | $2,088 PSF |

| EC project example: Tampines Street 95 EC | 560 units planned |

| Upcoming EC sites announced in GLS 1H 2025 | 10 sites, including three EC sites |

The market indicates a strong preference for ECs due to their balance of affordability and private housing qualities. Resale EC units fetching above $1 million have become increasingly common, reflecting the high demand and appreciation potential of these properties.

Notably, HDB upgraders drive a large portion of EC purchases, leveraging the wealth created by HDB resale profits as down payments for these developments.

What Is the Difference Between Executive Condo (ECs) and Condos?

Eligibility

Singaporean family nucleus; household income ≤S$16,000/month

No restrictions; open to locals and foreigners

Financing

Bank loan only; subject to MSR (30%) and TDSR (55%)

Bank loan only; TDSR applies

Grants

Eligible for CPF Housing Grant (up to S$30,000)

Not eligible

Minimum Occupation Period (MOP)

Five years before resale or full rental

None

Resale Rules

Years 6 to 10: sell only to SC/PRAfter 10 years: fully privatised

No restrictions; can sell anytime

Price Range (2025)

Launches from ~S$1,500 to S$1,700 psf

Typically S$1,900 to S$2,400 psf in OCR/RCR

Location

Mostly non-mature or fringe towns (e.g. Woodlands, Tengah)

Across all regions, including central districts

Ownership Appeal

Hybrid housing – ideal for first-time upgraders

Premium option for investors or high-income buyers

Rental Flexibility

Restricted during MOP

No restrictions

Capital Gain Potential

Often rises after the 10th year (when privatised)

Depends on market and location; usually steadier

2025 Trend Highlights

Record EC prices, shrinking discount vs private condos, high demand despite tight MSR

Stable resale demand, slower new-launch absorption in non-prime areas

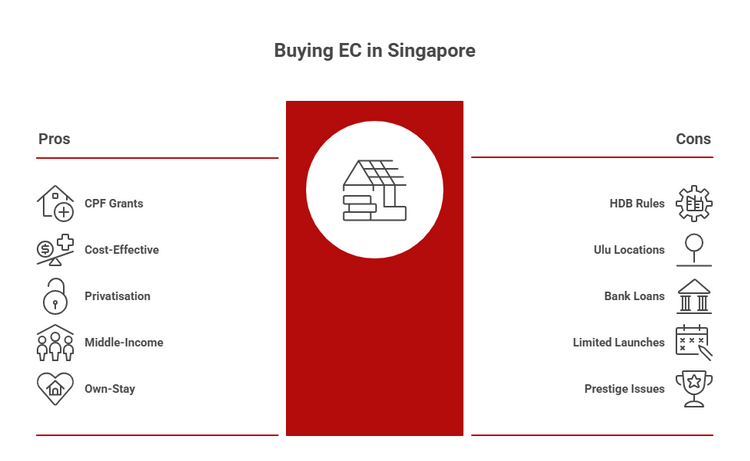

Pros of Buying ECs in Singapore (2025)

- Eligible for CPF Housing Grants

First-time EC buyers can receive CPF Family Grants (up to S$30,000) or Half-Housing Grants if one of the applicants has previously owned an HDB flat. These grants help reduce the overall purchase cost, making ECs an affordable entry into condo-style living.

- Cheaper Than Private Condos

ECs are typically 20% to 30% less than comparable private condos at launch. In 2025, EC prices average around S$1,500 to S$1,700 psf, while private condos in similar areas often exceed S$2,000 psf, offering buyers a more cost-effective alternative. - Privatised After 10 Years

ECs become fully privatised after their 10th year, meaning owners can sell or rent to foreigners without restrictions. This transition often results in a higher resale value as the property enters the private market segment. - Ideal for Middle-Income Buyers

With an income ceiling of S$16,000 per household, ECs are tailored for Singaporeans who earn too much for new HDB flats but find private condos out of reach. They offer a balanced option between affordability and lifestyle. - Designed for Own-Stay Buyers

EC purchase and resale conditions, including the five-year Minimum Occupation Period (MOP), encourage genuine owner-occupation. This helps maintain a stable, community-focused environment within developments.

Cons of Buying ECs in Singapore (2025)

- Bound by HDB Rules for 10 Years

ECs are considered public housing for the first 10 years, so owners must follow HDB regulations. This includes a five-year Minimum Occupation Period (MOP), during which you must reside in the unit before selling or renting it out, and limited resale options between years 6 and 10 (only to Singapore Citizens or Permanent Residents).

- Usually in Less Central (‘Ulu’) Areas

Most EC projects are built on lower-cost land in non-mature or fringe locations such as Tengah, Woodlands, or Sembawang. While this keeps prices affordable, daily commutes and access to amenities may be less convenient compared to central condos. - Financed Only Through Bank Loans

Can EC take hdb loan? EC buyers cannot use an HDB loan and must rely on bank financing, which typically requires a minimum 25% down payment (5% in cash, 20% in CPF/cash). Buyers also need to meet MSR (30%) and TDSR (55%) limits, which can cap borrowing power. - Limited EC Launches Each Year

EC land supply is tightly controlled by the government, resulting in new launches being few and highly competitive. In 2025, only a handful of EC sites were released, resulting in strong demand and rapid sellouts during the balloting process.

- ECs Face Prestige & Competition Post-Privatisation

After the 10-year privatisation period, ECs enter the open market and face competition from newer private condominium launches, often with more modern designs, advanced smart home features, and better locations.

Additionally, some buyers perceive ECs as less prestigious than private condos due to their public housing origins and restrictions that apply for the first 10 years.

Ready to buy an EC?

Browse executive condos and secure your ideal home today.

How To Buy an EC in Singapore (2025): Executive Condo Eligibility and More

Buying an Executive Condominium (EC) in Singapore is slightly more complex than purchasing a private condo, as it follows both HDB and private property rules. Here’s a complete step-by-step guide updated for 2025 to help you through the process.

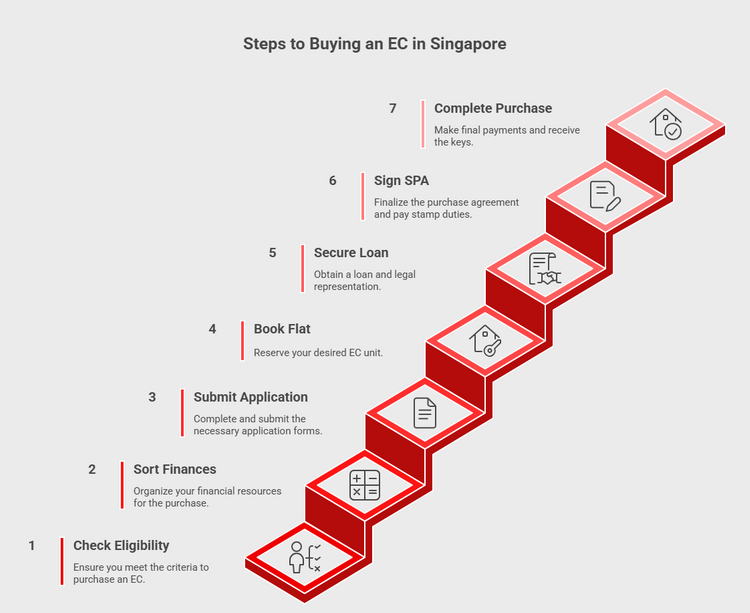

1. Executive Condo Eligibility

Before applying, make sure you meet the HDB eligibility criteria for ECs. These are the core EC requirements every applicant must fulfil.

| Criteria | Requirement |

| Eligible Applicant / Family Nucleus | You must qualify under at least one scheme: Public Scheme, Fiancé/Fiancée Scheme, or Orphans Scheme. |

| Citizenship | At least one applicant must be a Singapore Citizen, and at least one other must be a Singapore Citizen or Permanent Resident (SPR). |

| Age | Minimum 21 years old (for married, widowed, or orphaned applicants), or 35 years old if unmarried or divorced. |

| Income Ceiling | Combined household income must not exceed S$16,000 per month. |

| Property Ownership | You must not own, or have disposed of, any private property (local or overseas) in the past 30 months. You can only buy an EC twice in your lifetime. |

You must also not have bought more than one new HDB/DBSS flat or EC before, or received more than one CPF Housing Grant.

If you’re wondering, “Can singles buy ECs?” Yes, but with conditions. Singles can only apply under the Joint Singles Scheme for a new EC, or buy resale and fully privatised ECs on the open market. So check your resale EC eligibility before applying.

2. Sort Out Your Finances

Once eligibility is confirmed, the next step is to sort out your finances. Obtain an In-Principle Approval (IPA) from a bank; this indicates how much the bank is willing to lend you and helps set your property budget.

Your Loan-to-Value (LTV) ratio will depend on factors like your income, age, existing loans, and loan duration.

Other essential costs to factor in include:

- Buyer’s Stamp Duty (BSD)

- Option to Purchase (OTP) fee

- Legal fees

- Fire insurance

- HDB resale levy (if applicable)

3. Submit Your Application

When EC sales open, please check with the developer for the required documents, such as your NRIC, proof of income, and marital status. Once submitted, the developer will verify your eligibility and assign you a ballot number, which also indicates your unit selection appointment date.

4. Book Your Flat

During your appointment, visit the show flat and choose your preferred unit. If your preferred choice is unavailable, you may withdraw without penalty.

If you decide to proceed, you must present a cheque to the developer for the 5% booking fee, payable in cash, to secure your Option to Purchase (OTP).

You’ll then receive the Property Details Information (PDI) documents, including floor plans, site plan, and the Sale and Purchase Agreement (SPA). Read them carefully before signing.

Afterwards, HDB will review your application, which may take up to four weeks. If you plan to use CPF funds, submit the CPF Withdrawal Form RPS/1A (Residential Properties Scheme).

5. Hire a Conveyancing Lawyer, Secure Your Loan, and Obtain a Letter of Offer

Once you receive the OTP, you’ll need to:

- Engage a conveyancing lawyer

- Provide your OTP copy to both your lawyer and the bank.

- Request loan quotes from different banks to compare interest rates and packages.

Ensure that you do not sign the Letter of Offer (LO) until your EC application is officially approved, as failure to do so may result in cancellation fees.

6. Sign the SPA and Pay Stamp Duties

After HDB approval, you’ll receive your SPA. You must exercise your option within three weeks and pay the remaining EC downpayment, which can be done via CPF.

This payment must be made when signing the SPA or within nine weeks of signing the OTP, whichever is later.

Finally, pay the Buyer’s Stamp Duty (BSD) within two weeks of signing the SPA. If you decide not to proceed, 25% of your booking fee will be forfeited.

Unsure how much stamp duty to pay?

Use our Stamp Duty Calculator for a quick and accurate estimate.

7. Wait for Completion and Make the Remaining Payments

Once you’ve exercised your SPA, you’ll choose between two payment options:

Progressive Payment Scheme (PPS)

- Pay the 5% option fee in cash when booking the unit.

- Sign the Sale & Purchase Agreement (SPA) and pay the remaining 15% EC downpayment – CPF savings can be used for this.

- Settle the Buyer’s Stamp Duty (BSD) and, if applicable, the Additional Buyer’s Stamp Duty (ABSD). Both can also be paid using CPF funds.

Payments are made as construction progresses.

| Construction Stage | Approx. % of Purchase Price |

| Foundation work | 10% |

| Reinforced concrete framework | 10% |

| Partitions and walls | 5% |

| Ceilings | 5% |

| Internal plastering, plumbing, wiring, etc. | 5% |

| Roads, drains, and car parks | 5% |

| Temporary Occupation Permit (TOP) issued | 25% |

| Final completion (CSC issued) | 15% |

| Total | 80% |

Deferred Payment Scheme (DPS)

You’ll pay 20% upfront (5% OTP + 15% SPA) and the remaining 80% only upon TOP. However, ECs under the Deferred Payment Scheme (DPS) usually cost more.

This scheme appeals to those servicing an existing mortgage, as it offers more time to manage repayments before taking on a new full loan.

Find Your Ideal Home Effortlessly

Stop searching endlessly. Save your favourite properties and get curated listings directly on our app.

Can I Buy EC If I Own HDB Flat? (2025)

If you already own an HDB flat, you may be checking who can buy EC while still holding an existing property. The rule is that you must sell your flat before collecting the keys to your new EC.

This is because new ECs are treated as public housing during their first 10 years, and HDB does not allow ownership of two subsidised properties at the same time.

Here’s what you need to know in 2025:

- You can apply for a new EC while still owning your HDB flat, but you must dispose of your flat within six months after receiving the keys to your EC.

- If your current HDB flat is a BTO or resale flat bought with a CPF Housing Grant, you’ll also need to pay a resale levy when buying the new EC.

- The resale levy ranges from S$15,000 to S$55,000, depending on your previous flat type. It’s deducted from your CPF or cash proceeds.

- If you’re buying a resale or privatised EC, you don’t need to sell your HDB flat before the purchase since these properties are no longer under HDB’s public housing rules.

- Make sure you’ve fulfilled the five year Minimum Occupation Period (MOP) of your existing HDB flat before applying for a new EC. You cannot apply for a new EC while still within your MOP.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.