If you’re looking for a clear HFE application guide, you’re in the right place. The HDB Flat Eligibility (HFE) letter gives you an overview of your HDB flat eligibility, CPF Housing Grant eligibility and amounts, and your HDB loan eligibility with the loan quantum. For second-timers, the HFE letter also shows the resale levy amount.

In this guide, you’ll learn who needs an HDB HFE letter, how to apply for it, and how to check your HFE application status.

Table of Contents

1. What Is the HFE Letter?

2. Why You Need an HFE Letter in 2025?

3. HFE Letter Application: How the Process Works

4. How Long Does HFE Take?

5. How to Check HFE Application Status?

6. Step-by-Step Guide: How to Download HFE Letter

7. HFE Letter vs HLE: What Changed?

8. What to Do if Your Application Is Rejected?

1. What Is the HFE Letter?

2. Why You Need an HFE Letter in 2025?

3. HFE Letter Application: How the Process Works

4. How Long Does HFE Take?

5. How to Check HFE Application Status?

6. Step-by-Step Guide: How to Download HFE Letter

7. HFE Letter vs HLE: What Changed?

8. What to Do if Your Application Is Rejected?

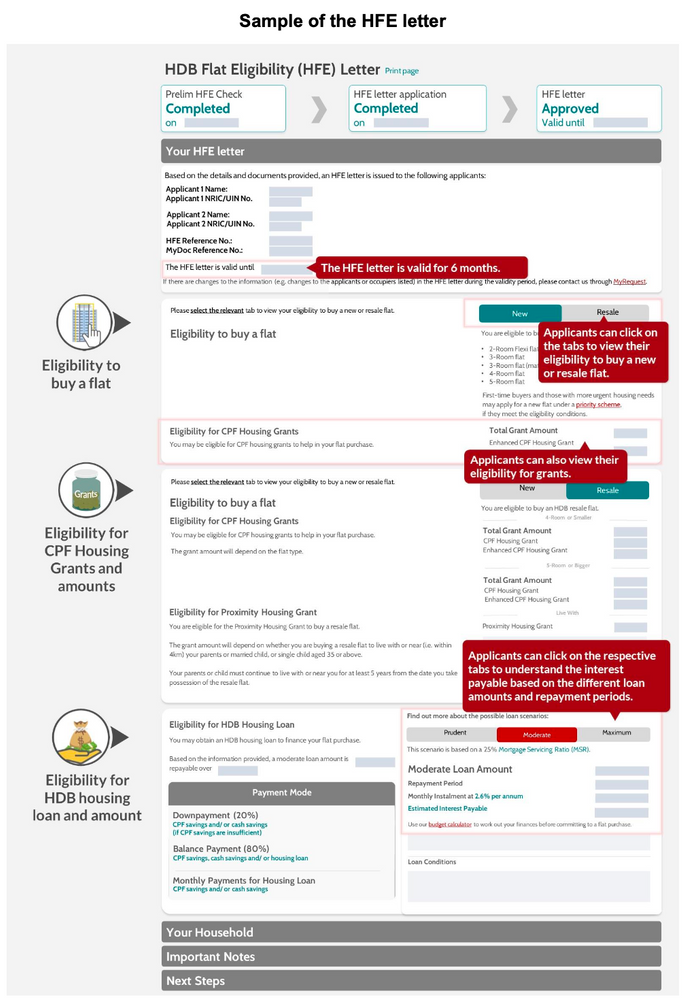

What Is the HFE Letter?

The HFE Letter in 2025 stands for the HDB Flat Eligibility letter. It is an all-in-one document issued by the Housing & Development Board (HDB) that summarises a prospective buyer’s eligibility to purchase a new or resale flat, their eligibility for housing grants, and their qualification for an HDB housing loan.

The HFE letter is essential for applying for BTO flats during sales exercises or obtaining an Option To Purchase (OTP) for resale flats. It was introduced as a new and improved version to replace the earlier HLE (HDB Loan Eligibility) letter on 9 May 2023, broadening the assessment to include flat purchase, grants, and loan eligibility in a single streamlined document.

Applicants typically apply for the HFE letter early in their house-hunting journey by logging in to the HDB Flat Portal via SingPass and providing relevant information, such as CPF contributions and income details. The HFE letter is also required before participating in sales exercises such as BTO or resale flat applications, to establish eligibility upfront and assist buyers in making informed housing and financing decisions.

Not sure what you can afford?

Get quick answers with our home loan tools and calculators.

Why Do You Need an HFE Letter in 2025?

You need an HFE (HDB Flat Eligibility) letter in 2025 because it is the official document that confirms your eligibility to buy a new or resale HDB flat, including your eligibility for housing grants and the ability to take an HDB housing loan. It streamlines the application process by consolidating flat purchase eligibility, grant qualification, and loan eligibility into a single letter, which you must have before applying for BTO or resale flats.

Having the HFE letter helps you:

- Confirm upfront whether you qualify for an HDB flat and related financial assistance.

- Ensure eligibility for various housing grants that can reduce your flat purchase cost.

- Determine if you can secure an HDB housing loan to finance your purchase.

- Participate in flat sales exercises with confidence and meet HDB requirements.

- Make informed decisions about budgeting and financing your home purchase.

In essence, the HFE letter is an essential preliminary step that provides clarity on your flat buying options, eligibility status, and financing possibilities before you commit to applying for or buying a flat in 2025.

Affordable homes with great amenities.

Discover HDB flats for sale near you.

HFE Letter Application: How the Process Works

The process to apply for the HFE (HDB Flat Eligibility) letter in 2025 involves several straightforward steps designed to assess your eligibility for purchasing an HDB flat, housing grants, and HDB loans. Here’s how it typically works:

- Prepare Your Information: Before applying, gather relevant details such as your employment records, income proof, CPF contribution history, and any other documents required to confirm your financial status.

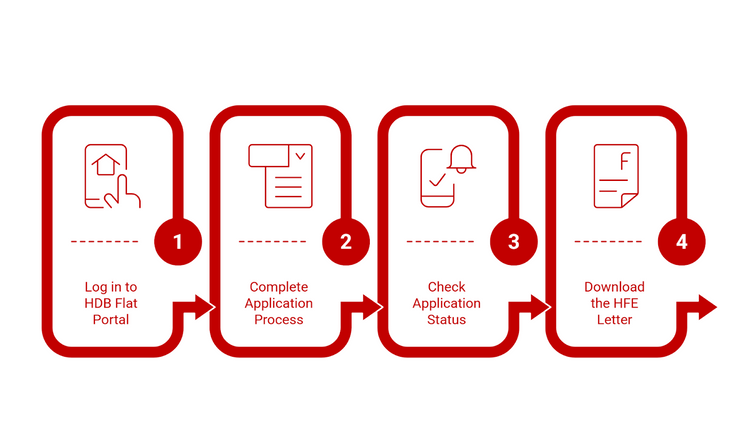

- Log In to the HDB Flat Portal: Access the official HDB Flat Portal using Singpass for secure login. This portal is the primary platform to submit your HFE application online.

- Submit Your Application: Complete the application form on the portal, providing accurate, up-to-date information about your household income, personal particulars, and other eligibility details. You may also declare your intention to apply for an HDB loan or grants.

- Income Assessment Period: Your income will be assessed based on the 12 months ending two months before your application month. It means HDB checks your recent income status to determine eligibility.

- Receive the HFE Letter: Once processed, HDB issues the HFE letter, which details your eligibility to buy a flat, qualify for grants, and obtain an HDB housing loan.

- Use the HFE Letter: With this letter, you can participate in BTO sales exercises, apply for resale flats, or proceed with flat purchase decisions knowing your eligibility status upfront.

If your circumstances change (e.g., income or household size), you may need to reapply to update your eligibility status. This system helps buyers plan and budget more effectively by consolidating key eligibility information into a single official document.

How Long Does HFE Take?

If you’re wondering “HFE letter how long?”, the processing time is usually about 21 working days (approximately one month) after HDB receives your complete application and all required documents.

This processing time might be shorter if your documents are complete from the start, sometimes about a week, but during peak periods, such as before or during BTO sales launches, it can take longer. You will be notified via SMS when your HFE letter is ready for download on the HDB Flat Portal.

To avoid delays, it is advisable to apply early, ideally at least 15 working days before a BTO or sale launch exercise. If you submit incomplete documents, HDB will request the missing information, which can extend the processing time.

How to Check Your HFE Application Status

To check the status of your HFE (HDB Flat Eligibility) letter application in 2025, follow these steps:

- Log in to the HDB Flat Portal using your Singpass credentials.

- Navigate to "My Flat Dashboard" within the portal.

- Select the section for "Applying an HDB Flat Eligibility (HFE) Letter" or your HFE application.

- Your application status, including any updates or requests for additional documents, will be displayed here.

- HDB will also notify you via SMS and email when your HFE letter is ready for viewing and download.

- If additional documents are required or the application encounters issues, you will receive instructions through these notifications.

This portal allows you to conveniently track the progress of your HFE application and stay informed about any next steps needed to complete your flat eligibility process.

Step-by-Step Guide: How to Download HFE Letter

To download your HFE (HDB Flat Eligibility) letter in 2025, follow these steps:

- Log in to the HDB Flat Portal: Use your Singpass account to access the portal. You can do this via the official HDB website or portal.

- Complete the Application Process:

- If you haven’t applied yet, you’ll need to fill in your personal details, household particulars, income information, and declare any private property ownership.

- Submit any required supporting documents, such as your CPF contribution history and Notices of Assessment from IRAS.

- Check Application Status:

- After submission, HDB usually takes about 21 working days to process your application, though processing times may be longer during peak periods.

- You will receive an SMS notification once your HFE letter is ready.

- Download the HFE Letter:

- Log back into the HDB Flat Portal.

- Go to your application status page to view the issued HFE letter.

- Download and save the document for your records and future use in flat applications.

Remember, the HFE letter is valid for nine months from the date of issuance, so plan your flat purchase within this period.

HFE Letter vs HLE: What Changed?

Here is a detailed comparison table between the HFE (HDB Flat Eligibility) letter and the HLE (HDB Loan Eligibility) letter as of 2025 to clarify the differences and changes:

Purpose

Assessed eligibility for an HDB housing loan only

Assesses eligibility for flat purchase, housing grants, and the HDB housing loan in one consolidated letter.

Eligibility Covered

Only HDB housing loan eligibility

Flat purchase eligibility (BTO/resale), CPF housing grants, and HDB housing loan eligibility

Application Timing

For BTO: after queue number and before flat booking

For resale flats: before obtaining the Option to Purchase (OTP)

For resale flats: before obtaining the Option to Purchase (OTP)

Must be applied for before any BTO or resale flat application, or before getting an OTP

Income Assessment Period

Six months before the application date

12 months ending two months before the application month

Validity Period

Six months

Nine months

Consolidation of Processes

Needed separate HLE letter for loan, separate applications for grants and flat eligibility checks

One-stop letter consolidating eligibility for loans, grants, and flat purchase

Convenience

Multiple letters and applications are required at different stages

Streamlined application process with all eligibility info upfront

Requirements

Only assessed loan eligibility details: loan amount, repayment period, and monthly instalments

Assesses eligibility to buy, grants available, loan amount, and financing options

Extra Information Provided

Amount of cash proceeds from the previous flat sale for second-home buyers

Comprehensive eligibility for flat type, grants, and loans

Impact on Home Buyer Planning

Limited scope; buyers had to apply multiple times at different stages for eligibility info

Comprehensive upfront information helps buyers plan finances and eligibility from the start.

The HFE letter was introduced to simplify and unify the home-buying eligibility process in Singapore, replacing the older HLE letter system in May 2023. It helps property buyers by providing a complete eligibility assessment for flat purchase, grants, and loans in a single streamlined document, making the process more transparent and more efficient for 2025 buyers.

Find the perfect upgrade for your lifestyle.

Check out HDB Executive Apartments for sale.

What if Your HFE Application Is Rejected?

Here is a detailed walkthrough of the following steps, appeals, and how to fix eligibility issues if your HDB Flat Eligibility (HFE) letter application is rejected in 2025:

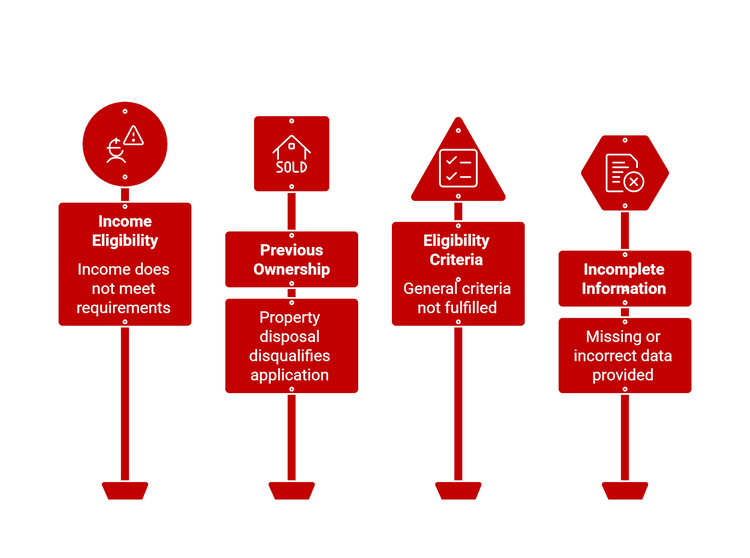

Common Reasons for Rejection

- Income Eligibility Not Met: Your household income does not meet the thresholds set for the flat types or grants you applied for. For example, households with no income in the assessed 12-month period preceding the application (e.g., students without income) may be deemed ineligible at the time of application.

- Previous Ownership or Disposal of Property: You may be disqualified if you or any family member has owned or sold a private property or HDB flat within the last specified period (usually 30 months or more, depending on scheme rules).

- Non-fulfilment of Eligibility Criteria: Issues like non-citizen buyers who don’t meet minimum requirements, failure to meet family nucleus or other profile conditions.

- Incomplete or Incorrect Information: Errors or missing documents submitted with the application can result in rejection or delay.

Next Steps After Rejection

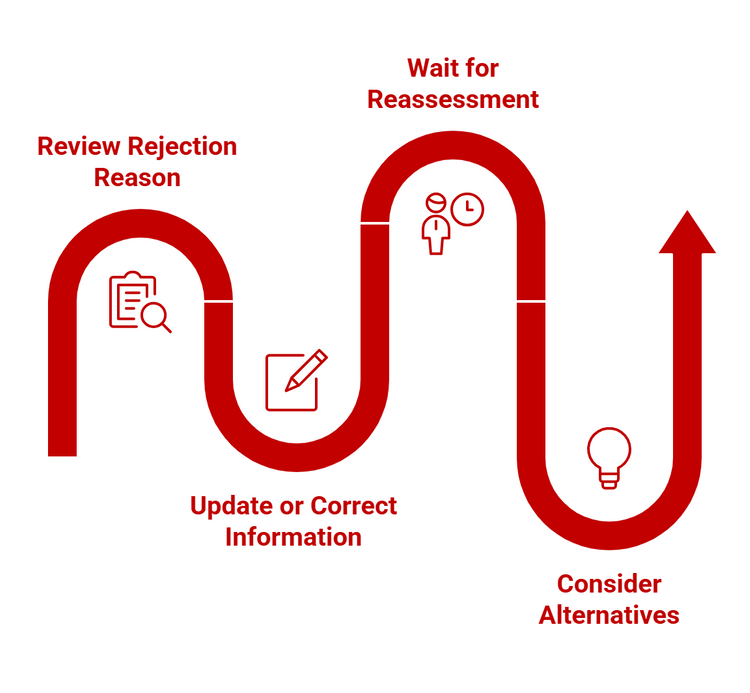

- Review the Rejection Reason: The HDB letter or notification should specify why eligibility was denied. Carefully review their feedback and see whether it aligns with your financial or personal situation.

- Update or Correct Information: If your application was rejected due to incorrect or incomplete details, gather the correct documents and resubmit the application or update your information through the HDB Flat Portal.

- Wait for Income Eligibility to be Reassessed: For cases where income was not available during the assessed period (e.g., students or those recently unemployed), eligibility for grants and loans can be reassessed later, usually around key collection or at the resale purchase stage once evidence of income or employment is available.

- Consider Alternative Flat Types or Eligibility: If rejected for certain flat types or grants, consider applying for flats with different income ceilings or eligibility requirements that you qualify for.

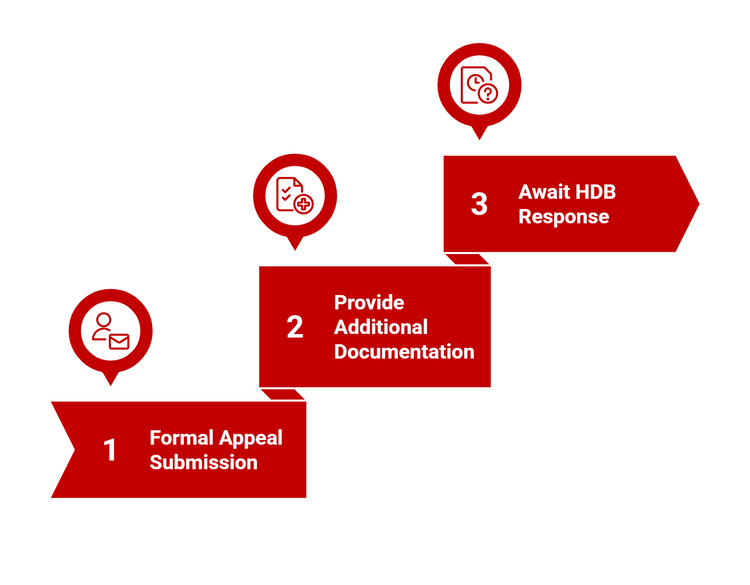

Appeals Process

- Formal Appeal Submission: If you believe the rejection was in error, you can submit a formal appeal via HDB’s official channels. This can be done through the HDB Flat Portal or by contacting an HDB branch to explain your case and provide supporting evidence.

- Provide Additional Documentation: Appeal success often depends on submitting additional proof to clarify your eligibility, such as recent income documents, employer letters, or legal declarations of household status.

- Await HDB Response: The review process may take several weeks. HDB will communicate their decision once the appeal is processed.

Other Support and Advisory

- Seek Customer Support: If you encounter technical difficulties during the application or need clarification, you can contact HDB customer service or visit a nearby branch for assistance.

- Plan for Reapplication Timeline: If your appeal or reapplication takes time, plan future flat applications accordingly to avoid missing BTO or resale flat sales exercises.

By following these steps, applicants can address rejection reasons effectively, ensure their information is accurate, and potentially appeal or reapply with a better chance of eligibility.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.