Buying a private condominium often starts with one big question. How much cash is needed upfront? Many buyers only realise later that the downpayment is not just a simple percentage. It depends on loan limits, CPF usage, and timing. Small gaps in understanding can lead to stress, delays, or missed opportunities.

In 2026, the rules around the downpayment for condo purchases remain strict. At the same time, prices stay high, and financing conditions continue to matter. Buyers need clarity before committing, not after signing documents.

This guide explains how condo downpayments work in Singapore today. It breaks down how much is needed, what must be paid in cash, and when payments are due. It also covers resale units and foreign buyers. The aim is simple: to help buyers plan with confidence and avoid costly surprises.

Table of Contents

1. Understanding The Downpayment For Condominiums In Singapore

2. What Affects the Cost of Condo Downpayment in Singapore?

3. How Much Downpayment For a Condominium Is Required In 2026?

4. What First-Time Condominium Buyers Should Know About Downpayment?

5. How Much Cash Buyers Need Upfront for a Condominium?

6. Case Study: Upfront Costs When Buying A Condominium In Singapore

7. Buying A Condominium In Singapore: Upfront Cost For Singapore Citizens

8. Buying A Condominium In Singapore: Upfront Cost For Singapore Permanent Residents

9. Buying A Condominium In Singapore: Upfront Cost For Foreigners

10. When to Pay Downpayment for a Condominium?

11. How Much Downpayment Is Needed for a Resale Condo Purchase?

12. What Upfront Costs Are There Besides The Downpayment?

13. Ready To Plan Your Condominium Downpayment With Confidence?

1. Understanding The Downpayment For Condominiums In Singapore

2. What Affects the Cost of Condo Downpayment in Singapore?

3. How Much Downpayment For a Condominium Is Required In 2026?

4. What First-Time Condominium Buyers Should Know About Downpayment?

5. How Much Cash Buyers Need Upfront for a Condominium?

6. Case Study: Upfront Costs When Buying A Condominium In Singapore

7. Buying A Condominium In Singapore: Upfront Cost For Singapore Citizens

8. Buying A Condominium In Singapore: Upfront Cost For Singapore Permanent Residents

9. Buying A Condominium In Singapore: Upfront Cost For Foreigners

10. When to Pay Downpayment for a Condominium?

11. How Much Downpayment Is Needed for a Resale Condo Purchase?

12. What Upfront Costs Are There Besides The Downpayment?

13. Ready To Plan Your Condominium Downpayment With Confidence?

Planning your property budget?

Find out your monthly mortgage repayments instantly.

Understanding The Downpayment For Condominiums In Singapore

The downpayment is the upfront amount paid when buying a private condominium. It is separate from the housing loan and must be prepared before the purchase can move forward.

The downpayment for condo purchases is shaped by loan rules set by the Singapore Government and banks. The amount required is not fixed. It depends on several factors, including:

- The loan-to-value limit set by the bank

- Whether the buyer has an existing housing loan

- How much CPF savings can be used

Many buyers assume the downpayment is a flat figure. That is not always the case. The required amount can change based on the buyer’s profile and financing choice.

At a basic level, the downpayment determines how much cash and CPF savings must be ready before signing any agreement. This makes it one of the most important costs to plan for when buying a private condominium.

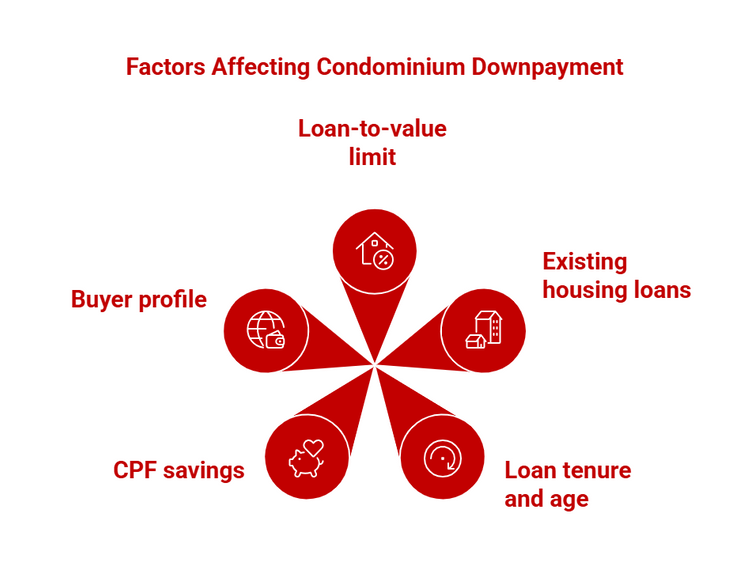

What Affects the Cost of Condo Downpayment in Singapore?

The downpayment amount for a private condominium is not the same for every buyer. It changes based on financing rules and the buyer’s profile. Understanding these factors early helps avoid last-minute funding gaps.

The main factors that affect how much downpayment is required include:

- Loan-to-value limit: This is the maximum percentage a bank can lend. A lower loan-to-value limit means a higher downpayment.

- Number of existing housing loans: Buyers with one or more existing housing loans face stricter loan limits. This increases the upfront amount required.

- Loan tenure and borrower’s age: Longer loan tenures or loans extending beyond age sixty-five can reduce the loan-to-value limit. This leads to a higher downpayment.

- Use of CPF savings: CPF Ordinary Account savings can be used for part of the downpayment if eligible. This affects how much cash needs to be prepared.

- Buyer profile: Foreign buyers cannot use CPF. This means the full downpayment must be paid in cash.

Because these factors interact, two buyers purchasing similar units may face very different upfront costs. This is why understanding the structure comes first. The actual downpayment figures make more sense once these variables are clear.

How Much Downpayment For a Condominium Is Required In 2026?

For most buyers, the downpayment is linked directly to the Loan-to-Value (LTV) limit set by MAS. The LTV depends on the number of existing housing loans, the chosen loan tenure, and the borrower’s age.

Use the table below as a planning guide.

No existing housing loan

75% or 55%*

25%

5% if LTV = 75% ; 10% if LTV = 55%.

One existing housing loan

45% or 25%*

55%

25% cash.

Two or more existing loans

35% or 15%*

65%

25% cash.

*Take the lower LTV where the loan tenure exceeds 30 years (or 25 years for HDB) or if the loan extends beyond the borrower’s 65th birthday.

Notes and practical points

- The downpayment shown is the portion not financed by the bank. For example, a 25% downpayment on a S$1,000,000 unit equals S$250,000. Of that, a specified minimum must be paid in cash; the remainder may be paid from cash or CPF Ordinary Account savings, where eligible.

- Banks may apply lower LTVs for conservative underwriting. The final LTV granted can be lower than the regulatory maximum, depending on income, credit profile, and other loans. Plan for this possibility.

- Foreign buyers cannot use CPF and face higher upfront cash requirements because CPF OA is unavailable to them. They also pay ABSD, which increases the total cash required at the time of purchase.

- New launches may follow a staged payment schedule. Initial deposits and option exercise payments form part of the total downpayment structure. See the project payment schedule when budgeting.

Understanding how much downpayment for condo in Singapore is required helps buyers assess affordability early. It also reduces the risk of delays when securing financing or committing to a purchase.

What First-Time Condominium Buyers Should Know About Downpayment?

Many buyers assume that purchasing a private condominium for the first time comes with lower upfront requirements. In Singapore, this is a common misunderstanding. First-time status does not change the downpayment rules for private property.

For buyers with no existing housing loan, banks may lend up to 75% of the property price, subject to eligibility. This means the downpayment for condo purchases starts at 25% of the purchase price.

Typical downpayment structure for first-time buyers:

| Item | Requirement |

| Maximum loan-to-value | 75% |

| Total downpayment required | 25% |

| Minimum cash downpayment | 5% |

| Balance downpayment | Cash or CPF Ordinary Account savings |

This structure applies only when the buyer qualifies for the maximum loan-to-value limit.

If the loan tenure exceeds 30 years, or if the loan extends beyond the borrower’s sixty-fifth birthday, the maximum loan may be reduced to 55%. In this case, the downpayment rises to 45%, with a higher minimum cash portion.

When Downpayment Requirements Increase

| Scenario | Impact On Downpayment |

| Loan tenure over 30 years | Lower loan-to-value limit |

| Loan extends beyond age sixty-five | Higher downpayment required |

| CPF balance is insufficient | Additional cash needed |

It is also important to separate downpayment rules from stamp duty treatment. While first-time buyers may benefit from lower stamp duties, this does not change how much downpayment for condo in Singapore is required.

Understanding these details early helps first-time buyers plan realistically and avoid cash shortfalls later in the purchase process.

How Much Cash Buyers Need Upfront for a Condominium?

Seeing percentages is helpful, but many buyers want to know what the numbers look like in real terms. This worked example shows how the downpayment for condo purchases and other upfront costs can differ based on buyer profile.

Assumptions used for this example:

- Purchase price: S$800,000

- Bank loan with a 75% loan-to-value limit

- No existing housing loan

- Figures are indicative and for planning only

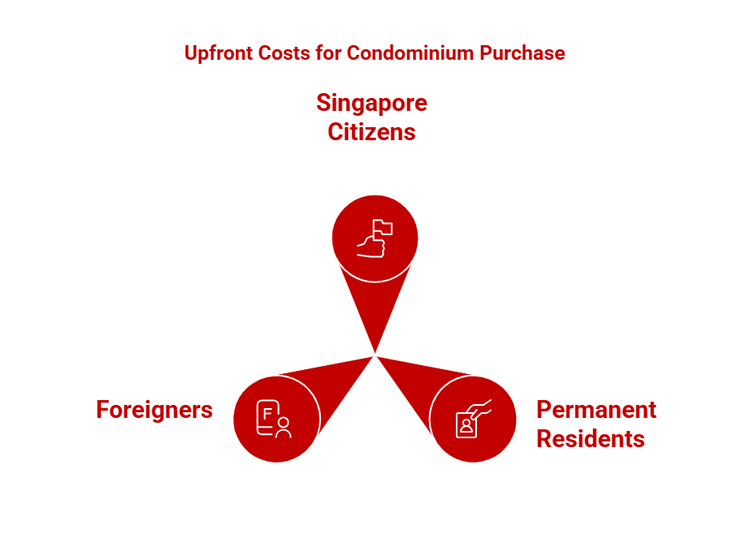

Estimated Upfront Costs By Buyer Profile:

Singapore Citizen

S$200,000 (25%)

S$40,000 (5%)

Allowed

Buyers’ Stamp Duty applies

At least S$40,000 plus stamp duties

Permanent Resident

S$200,000 (25%)

S$40,000 (5%)

Allowed

Buyers’ Stamp Duty and Additional Buyers’ Stamp Duty apply

At least S$40,000 plus stamp duties

Foreigner

S$200,000 (25%)

S$200,000 (full amount)

Not allowed

Buyers’ Stamp Duty and higher Additional Buyers’ Stamp Duty apply

Entire downpayment plus stamp duties

Notes:

- The downpayment for condo purchases is the portion not covered by the bank loan. It is separate from stamp duties and legal fees.

- The minimum cash downpayment for condo purchases applies to eligible buyers using bank loans. Any shortfall in CPF savings must be covered with additional cash.

- Foreign buyers cannot use CPF. As a result, the entire downpayment must be paid in cash.

- Stamp duties are paid separately and can significantly increase the total cash needed at completion.

This example highlights why buyers often use a downpayment for condo calculator early in the planning stage. While actual figures vary by property price and buyer profile, understanding the structure helps buyers estimate how much cash is needed before committing.

Case Study: Upfront Costs When Buying A Condominium In Singapore

The examples below are based on a typical private condominium purchase and are meant to help buyers plan realistically.

Assumptions Used For All Examples

- Purchase price: S$2 million

- Bank loan used where applicable

- No existing housing loan unless stated

- Maximum loan-to-value applies unless restricted by age or loan tenure

- Stamp duty rates reflect the current 2025–2026 rules

- Figures are indicative and for planning only

Buying A Condominium In Singapore: Upfront Cost For Singapore Citizens

The table below shows the estimated upfront costs for Singapore citizens buying a private condominium under different loan scenarios.

First condominium

75%

S$500,000

S$100,000

S$69,600

Not applicable

S$169,600 plus

First condominium, lower LTV applies*

55%

S$900,000

S$200,000

S$69,600

Not applicable

S$269,600 plus

Second condominium

45%

S$1,100,000

S$500,000

S$69,600

20% (S$400,000)

S$969,600 plus

Second condominium, lower LTV applies*

25%

S$1,500,000

S$500,000

S$69,600

20% (S$400,000)

S$969,600 plus

* Lower loan-to-value applies if the loan tenure exceeds 30 years or the loan runs beyond the borrower’s age of sixty-five.

Buying A Condominium In Singapore: Upfront Cost For Singapore Permanent Residents

The table below outlines how the downpayment and stamp duties apply to Singapore permanent residents when purchasing a private condominium.

First condominium

75%

S$500,000

S$100,000

S$69,600

5% (S$100,000)

S$269,600 plus

First condominium, lower LTV applies*

55%

S$900,000

S$200,000

S$69,600

5% (S$100,000)

S$369,600 plus

Second condominium

45%

S$1,100,000

S$500,000

S$69,600

30% (S$600,000)

S$1,169,600 plus

Second condominium, lower LTV applies*

25%

S$1,500,000

S$500,000

S$69,600

30% (S$600,000)

S$1,169,600 plus

* Lower loan-to-value applies if the loan tenure exceeds 30 years or the loan runs beyond the borrower’s age of sixty-five.

Buying A Condominium In Singapore: Upfront Cost For Foreigners

The table below shows the estimated upfront costs foreign buyers may face when purchasing a private condominium in Singapore, including the down payment for condo for foreigners under different loan scenarios.

Any condominium purchase

75%

S$500,000

S$500,000

S$69,600

60% (S$1,200,000)

S$1,769,600 plus

Lower LTV applies*

55%

S$900,000

S$900,000

S$69,600

60% (S$1,200,000)

S$2,169,600 plus

Foreign buyers cannot use CPF. This means the entire downpayment must be paid in cash.

* Lower loan-to-value applies if the loan tenure exceeds 30 years or the loan runs beyond the borrower’s age of sixty-five.

Important Notes For Readers

- Downpayment refers only to the portion not covered by the bank loan.

- Stamp duties are separate from the downpayment and must be paid in cash.

- The figures above exclude legal fees, valuation fees, and mortgage stamp duty.

- Actual loan amounts may vary depending on bank assessment and borrower profile.

These tables show why buyers often rely on a downpayment for condo calculator or a Singapore condo down payment calculator to estimate how much cash needs to be prepared before committing.

When to Pay Downpayment for a Condominium?

Understanding when the downpayment is paid is just as important as knowing how much to prepare. In Singapore, the payment timeline differs between resale condominiums and new launch condominiums.

Missing or misunderstanding a payment stage can delay the transaction or put the option at risk.

For Resale Condominium Purchases

Resale purchases follow a relatively short and fixed timeline.

Stage 1: Option To Purchase (OTP)

- When the seller grants the Option To Purchase, the buyer pays an option fee, usually 1% of the purchase price.

- This amount must be paid in cash and forms part of the total downpayment.

Stage 2: Exercising The Option

The buyer typically has 14 days to exercise the option.

At this stage, the buyer pays the balance of the downpayment, bringing the total paid to the required percentage based on the loan-to-value limit.

- CPF Ordinary Account savings can be used, if eligible

- Any shortfall must be paid in cash

Stage 3: Completion

Completion usually takes place eight to twelve weeks after the option is exercised.

The remaining balance of the purchase price is paid after the bank loan is disbursed.

By completion, the full downpayment and stamp duties must already be settled.

For New Launch Condominium Purchases

New launch purchases follow a staged payment structure, spread over a longer period.

Stage 1: Booking Fee

When a unit is booked, the buyer pays a booking fee of 5%, which must be paid entirely in cash.

This forms part of the downpayment.

Stage 2: Sale And Purchase Agreement

Within a few weeks, the buyer signs the Sale and Purchase Agreement.

At this point, the buyer pays the remaining portion of the downpayment, typically bringing the total to 25% for buyers qualifying for the maximum loan-to-value limit.

At this point, the buyer pays the remaining portion of the downpayment, typically bringing the total to 25% for buyers qualifying for the maximum loan-to-value limit.

- CPF Ordinary Account savings can be used, where eligible

- Any remaining amount must be paid in cash

Stage 3: Progressive Payments

After the downpayment is fully paid, the remaining purchase price is paid in stages based on construction milestones.

These payments are usually funded through the bank loan, once disbursed.

Key Points Buyers Should Note

- The cash portion of the downpayment is always paid first

- CPF can only be used after eligibility checks are completed

- Stamp duties are paid separately and are not part of the downpayment

- Buyers who do not qualify for the maximum loan-to-value limit must prepare a higher upfront amount earlier in the process

Understanding when to pay downpayment for condo purchases helps buyers plan cash flow properly. It also reduces the risk of delays at critical milestones, especially when CPF usage or loan approval timelines are involved.

How Much Downpayment Is Needed for a Resale Condo Purchase?

Resale condominium purchases follow the same loan rules as new launches, but the cash flow pressure is usually higher. This is because the payment timeline is shorter and the downpayment must be settled early in the process.

For buyers who qualify for the maximum loan-to-value of 75%, the downpayment for a resale condominium starts at 25% of the purchase price. The structure is the same as other private property purchases:

- Minimum 5% paid in cash

- The remaining 20% paid using the CPF Ordinary Account savings or cash

However, this applies only when the buyer has no existing housing loan and meets age and loan tenure requirements.

When The Downpayment Increases For Resale Purchases?

The downpayment for resale condominiums rises in the following situations:

- One existing housing loan: The maximum loan-to-value drops to 45%, increasing the downpayment to 55%. A larger portion of this must be paid in cash.

- Two or more existing housing loans: The loan-to-value may fall to 35% or lower, raising the downpayment to 65%.

- Loan tenure over 30 years or loan beyond age 65: The maximum loan-to-value may be reduced to 55%, increasing the downpayment to 45%.

Because resale purchases complete faster, buyers must have the full downpayment ready within weeks, not months. There is no progressive payment schedule to spread out the upfront cost.

Key Difference Between Resale And New Launch Purchases

For resale condominiums:

- The option fee and balance downpayment are paid within a short window

- CPF usage must be approved quickly to avoid delays

- Buyers need stronger upfront liquidity

For new launch condominiums:

- The downpayment is paid in stages

- Cash pressure is spread over a longer period

Understanding how much downpayment for resale condo purchases is required helps buyers avoid timing issues and funding gaps. It also ensures that loan approval and CPF usage are aligned before committing to the Option To Purchase.

Wondering how much home you can afford?

Check your budget and see what price range fits you.

What Upfront Costs Are There Besides The Downpayment?

The downpayment is only one part of the upfront cost when buying a private condominium. Buyers must also prepare for stamp duty and other charges payable early in the transaction. These costs are separate from the downpayment and must be paid in cash.

Buyers’ Stamp Duty Rates In Singapore

Buyers’ Stamp Duty is payable on all residential property purchases. It is calculated based on the purchase price or market value, whichever is higher.

Portion Of Property ValueBSD Rate

| Portion Of Property Value | BSD Rate |

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Next S$1.5 million | 5% |

| Amount above S$3 million | 6% |

Buyers’ Stamp Duty must be paid in cash and is due shortly after exercising the Option To Purchase.

Additional Buyers’ Stamp Duty Rates

Additional Buyers’ Stamp Duty applies depending on the buyer’s profile and the number of residential properties owned at the time of purchase.

Singapore Citizen

0%

20%

30%

Singapore Permanent Resident

5%

30%

35%

Foreigner

60%

60%

60%

Additional Buyers’ Stamp Duty is calculated on the full purchase price or market value and must be paid in cash. It often forms the largest portion of upfront costs for second-time buyers and foreign purchasers.

Other Common Upfront Costs

In addition to stamp duties, buyers should also budget for:

- Legal fees, which vary by law firm and transaction complexity

- Property valuation fees, usually a few hundred dollars

- Mortgage stamp duty, calculated on the loan amount

While these costs are smaller compared to stamp duties, they add to the total cash required before completion.

Understanding these rates helps buyers estimate their true upfront cost more accurately.

Buying a property soon?

Calculate your stamp duty payable and avoid surprises.

Ready To Plan Your Condominium Downpayment With Confidence?

Understanding the downpayment for condominium purchases removes much of the uncertainty from the buying process. Knowing how much to prepare, what must be paid in cash, and when payments are due helps avoid last-minute stress and financing delays.

Before committing to any unit, it is worth reviewing loan eligibility and CPF usage early. This gives a clearer picture of affordability and prevents surprises later in the transaction, which is why clear guidance around downpayment for condo PropertyGuru Singapore continues to matter for buyers.

For more guidance on private property financing, market updates, and buying steps in Singapore, explore the PropertyGuru Guides section.

If you are ready to take the next step, browse private condominium listings on PropertyGuru to compare prices, locations, and available options that match your budget and timeline.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.