Stamp duty plays a key role in why decoupling is often considered. Singapore Citizens pay 0% ABSD on their first property, 20% on the second property, and 30% on the third or subsequent properties, effective from 27 April 2023 and remaining unchanged through 2026.

Permanent Residents face 5% ABSD on the first property, 30% on the second, and 35% on the third and beyond, while foreigners are subject to 60% ABSD on any residential property.

Owning more than one property in Singapore often results in higher taxes, thereby increasing overall ownership costs. Many owners feel unsure about reducing stamp duty without compliance risks. This article explains the decoupling property clearly, covering decoupling tax in Singapore, how decoupling Singapore works, and what property owners should consider before deciding.

Table of contents

1. What Is Property Decoupling in Singapore?

2. What are the Additional Buyer’s Stamp Duty (ABSD) rules in 2026?

3. How does ABSD apply before and after decoupling the property?

4. How do buyer profiles and ownership statuses change after decoupling Singapore?

5. ABSD Rates in Singapore for 2026

6. What Are the Eligibility Rules for Decoupling Property?

7. What Common Mistakes Should Property Owners Avoid?

8. What Are the Alternatives to Decoupling Property?

1. What Is Property Decoupling in Singapore?

2. What are the Additional Buyer’s Stamp Duty (ABSD) rules in 2026?

3. How does ABSD apply before and after decoupling the property?

4. How do buyer profiles and ownership statuses change after decoupling Singapore?

5. ABSD Rates in Singapore for 2026

6. What Are the Eligibility Rules for Decoupling Property?

7. What Common Mistakes Should Property Owners Avoid?

8. What Are the Alternatives to Decoupling Property?

What Is Property Decoupling in Singapore?

Property decoupling in Singapore refers to a legal arrangement in which one co-owner transfers their share of a property to the other co-owner. This results in the property being held under a single name rather than in joint ownership. Decoupling is commonly discussed in the context of tax planning, especially for couples who plan to purchase another residential property while managing stamp duty costs.

- Decoupling meaning in simple terms

In simple terms, decoupling means one owner exits the property while the other becomes the sole owner. This is usually done through a sale-and-purchase transaction between the co-owners.

After decoupling, the person who transfers their share no longer owns any residential property, which may allow them to buy another home under their own name, subject to prevailing tax rules.

- Why do property owners consider decoupling?

Property owners often consider decoupling to manage their exposure to the Additional Buyer’s Stamp Duty (ABSD). In Singapore, ABSD increases significantly for second and subsequent property purchases.

By decoupling, one spouse may be treated as a first-time buyer when purchasing another property, potentially reducing the tax payable. Beyond tax planning, some owners also consider decoupling as part of long-term asset planning or family ownership structuring.

- How does decoupling work between spouses?

Decoupling between spouses typically involves one spouse buying out the other spouse’s share of the property at market value. This process requires legal documentation, property valuation, and bank approval if there is an existing housing loan.

CPF funds used for the original purchase must also be refunded where applicable. Once the transfer is completed, only one spouse remains on the title. At the same time, the other becomes free to purchase another property in their own name, subject to eligibility and financing conditions.

Ready to find your HDB flat?

Check out the latest HDB listings today.

What are the Additional Buyer’s Stamp Duty (ABSD) rules in 2026?

ABSD rules under Decoupling Singapore remain unchanged from the cooling measures introduced on 27 April 2023 and continue into 2026. ABSD is charged on top of BSD and depends on the buyer’s profile and the number of residential properties owned at the time of purchase.

ABSD rates in 2026:

- Singapore Citizens: 0% on first property, 20% on second, 30% on third or more

- Permanent Residents: 5% on first property, 30% on second, 35% on third and beyond

- Foreigners: 60% on any residential property

- Entities: 65% ABSD

- Developers: 40% ABSD (35% remittable and 5% non-remittable)

ABSD is calculated based on the higher of the purchase price or market value.

How does ABSD apply before and after decoupling the property?

Before decoupling the property, joint owners are each counted as owning one residential property. This directly affects the ABSD payable on any new purchase.

Before decoupling:

- Joint owners are treated as owning one property each

- A Singapore Citizen buying another property faces 20% ABSD

After decoupling:

- The outgoing owner transfers their share to the remaining owner

- Only BSD (1% to 6%) applies to the transferred share

- No ABSD is charged on the share transfer

- The outgoing owner’s property count becomes zero

This shift allows the outgoing owner to be assessed under first-property ABSD rules on a future purchase.

How do buyer profiles and ownership statuses change after decoupling Singapore?

After Decoupling Singapore is completed, ownership status is reassessed based on the registered title records held by the Singapore Land Authority. IRAS uses these records to determine ABSD eligibility.

Post-decoupling ownership impact:

- The outgoing owner is treated as owning zero residential properties

- Singapore Citizens may qualify for 0% ABSD on the next purchase

- Permanent Residents may qualify for 5% ABSD on the next purchase

- The remaining owner continues to be treated as owning one property

The decoupling arrangement must be genuine. Artificial or non-commercial structures may lead to ABSD being imposed retrospectively. CPF usage and housing loan eligibility are also reassessed based on the updated ownership profile.

Your ideal four-room HDB home is waiting.

Check out the latest listings in your preferred estate.

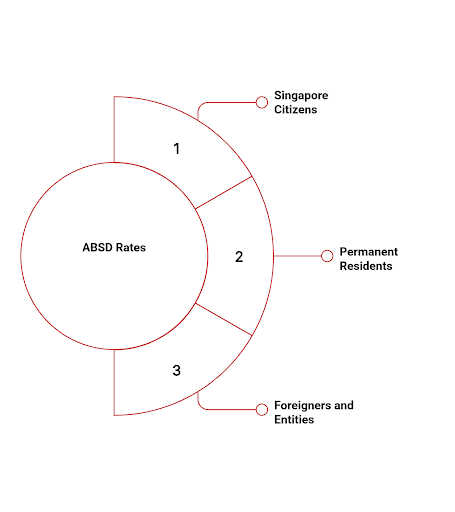

ABSD Rates in Singapore for 2026

Additional Buyer’s Stamp Duty rates under Decoupling Singapore remain unchanged from the cooling measures introduced on 27 April 2023 and continue to apply in 2026. ABSD is calculated based on the higher of the purchase price or market value and is charged in addition to Buyer’s Stamp Duty (BSD).

These rates depend on the buyer’s profile and the number of residential properties owned at the time of purchase, which is why ownership status play an important role in decoupling tax planning.

What is the ABSD for Singapore Citizens?

For Singapore Citizens, ABSD follows a progressive structure that increases with each additional property owned. This structure often drives interest in decoupling property strategies.

ABSD rates for Singapore Citizens in 2026:

- 0% ABSD on the first residential property

- 20% ABSD on the second residential property

- 30% ABSD on the third or subsequent residential properties

Under Decoupling Singapore, a citizen who legally owns zero properties after decoupling may qualify for the first-property ABSD rate on a new purchase.

What is the ABSD for Permanent Residents?

Permanent Residents face higher ABSD rates even on their first property, making ownership restructuring a common consideration when evaluating decoupling tax outcomes.

ABSD rates for Permanent Residents in 2026:

- 5% ABSD on the first residential property

- 30% ABSD on the second residential property

- 35% ABSD on the third or subsequent residential properties

After decoupling property, a Permanent Resident’s ABSD exposure depends on whether they are assessed as owning zero residential properties at the point of the next purchase.

What is the ABSD for foreigners and entities?

ABSD treatment is significantly stricter for foreigners and entities, regardless of ownership count, and does not reduce ABSD exposure for these buyer profiles.

ABSD rates for foreigners and entities in 2026:

- Foreigners pay 60% ABSD on any residential property purchase

- Entities are subject to 65% ABSD on any residential property

- Housing developers face 40% ABSD, made up of a 35% remittable portion and a 5% non-remittable portion

These rates apply uniformly and are assessed solely based on buyer profile, underscoring the importance of understanding how Decoupling Singapore affects ownership classification rather than buyer category.

What Are the Eligibility Rules for Decoupling Property?

Before considering decoupling, confirm that you meet the eligibility criteria. Many property owners focus on the decoupling tax benefits without realising that ownership rules, marital status, and property type can determine if decoupling is even allowed.

The decoupling meaning goes beyond mere paper transfers, as Decoupling Singapore follows specific legal and regulatory conditions. This section outlines the key eligibility rules that decide who can decouple, what properties qualify, and where restrictions may apply.

What marital status and ownership requirements apply to decoupling?

Eligibility for decoupling property in Singapore depends mainly on who owns the property and how the ownership is structured.

Decoupling is most commonly carried out between legally married spouses, as transfers between spouses are generally recognised under property and tax regulations. Both parties must already be listed as co-owners before decoupling can take place, and the transfer must reflect a genuine transaction.

Key eligibility points include:

- Co-owners are typically legally married spouses

- Both names must appear on the property title before decoupling

- One spouse buys over the other’s share through a proper sale process

- The remaining owner must qualify to hold the property under a single name

- Existing housing loans must be reassessed and approved by the bank

What property type restrictions affect the decoupling property?

Not every residential property qualifies for decoupling. The rules depend heavily on the type of property and the conditions attached to it.

Decoupling property is generally more straightforward for private homes, where ownership transfers are permitted under standard legal processes, subject to financing checks.

Common restrictions to consider:

- Minimum occupation period requirements

- Outstanding housing loans tied to joint ownership

- Ability of the remaining owner to service the loan alone

- Existing ownership conditions imposed at purchase

These factors must be carefully reviewed before proceeding, as they directly affect whether decoupling is permitted.

How do HDB and private property decoupling rules differ in Singapore?

Decoupling rules vary significantly between HDB flats and private properties under Decoupling Singapore. HDB flats are subject to stricter regulations, and decoupling is generally not permitted unless specific criteria are met and HDB approval is granted.

- HDB flats: Decoupling is usually restricted and allowed only under limited circumstances, such as changes in family structure or eligibility conditions

- Private properties: Greater flexibility, with ownership transfers allowed through standard conveyancing procedures

Because of these differences, understanding the property type is essential before assessing whether decoupling is a practical and compliant option.

Find a property that fits your needs.

Explore available homes and investments across top locations.

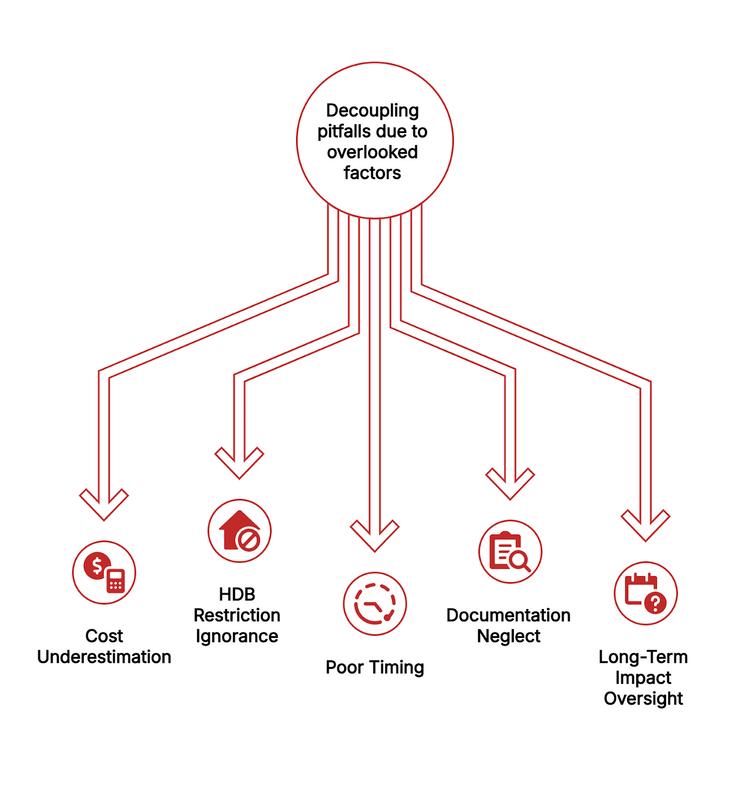

What Common Mistakes Should Property Owners Avoid?

Property owners in Singapore often overlook key pitfalls in ownership, especially when managing multiple properties or considering strategies such as decoupling, which can lead to unexpected costs or compliance issues. Common errors stem from underestimating taxes, ignoring restrictions, and poor planning.

- Underestimating Total Costs

Owners frequently calculate only purchase prices, missing stamp duties, legal fees, and refinancing costs post-decoupling. E.g., BSD on share transfers can exceed $ 10,000 for mid-range properties. Failing to budget for higher loan servicing under TDSR after one spouse assumes full ownership strains finances.

- Ignoring HDB Restrictions

Attempting to decouple HDB flats without qualifying under the six hardship categories results in rejection and wasted fees, as HDB has banned it for investment purposes since 2016. Owners also forget ethnic quotas or tenant eligibility when renting out post-decoupling properties.

- Poor Timing and SSD Risks

Selling shares before the four-year SSD exemption period triggers 12% duty on private properties, eroding decoupling savings. Rushing without legal advice can lead to invalid severance or to IRAS deeming it a sham, imposing retrospective ABSD.

- Neglecting Documentation and Insurance

Skipping proper handover inspections or tenancy agreements leads to disputes over damages; verbal deals are unenforceable. Private property owners often forget to take out home insurance, unlike HDB’s automatic coverage, leaving them exposed to tenant-related losses.

- Overlooking Long-Term Impacts

Assuming zero-property status lasts indefinitely ignores future buys, counting prior ownership; families risk CPF refund clawbacks if recombining later. Not checking credit reports pre-refinance delays approvals or worsens terms.

Careful planning, clear cost checks, and early legal advice help property owners avoid expensive mistakes and long-term issues.

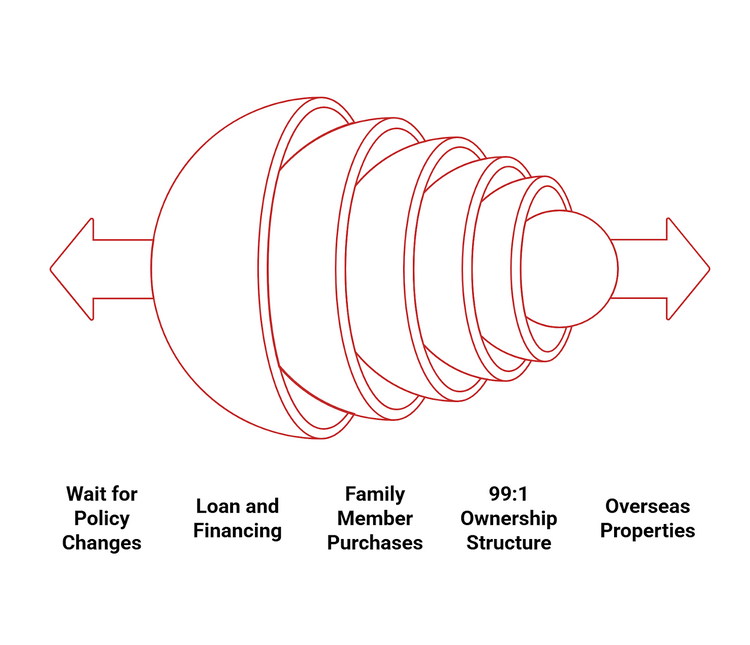

What Are the Alternatives to Decoupling Property?

Alternatives to decoupling allow Singapore property owners to expand portfolios or manage ownership without restructuring joint tenancy, often leveraging family structures, loans, or incentives amid high ABSD rates. These options suit different profiles, balancing costs, risks, and compliance with IRAS and HDB rules.

- 99:1 Ownership Structure

Couples initially buy properties with a 99:1 split, e.g., one spouse holds 99% and the other 1%, treated as one property each if correctly declared, enabling future purchases at lower ABSD rates without complete decoupling. The minority owner later transfers their 1% share post-MOP, paying minimal BSD, though IRAS flags the timing as potentially indicative of tax avoidance.

- Family Member Purchases

Parents or children buy properties under their profiles; e.g., adult children qualify as first-time buyers for 0% ABSD, or parents gift funds for separate titles within family units. This preserves household ownership limits but requires genuine transfers, avoiding sham arrangements scrutinised under anti-avoidance rules.

- Loan and Financing Strategies

Maximise Loan-to-Value (LTV) limits by refinancing existing loans or using bridging loans for sequential purchases, timing sales post-SSD exemption to fund new buys. ABSD remission applies to married couples selling one home within a year to buy another jointly, capped at first-property rates.

- Overseas or Commercial Properties

Invest in overseas residential properties exempt from Singapore ABSD, or in commercial real estate that does not count toward residential ownership caps. Entities like companies pay 65% ABSD on properties but enjoy corporate tax benefits; developers access 40% rates with remission potential.

- Wait for Policy Changes or Incentives

Monitor Budget announcements for ABSD reliefs, like past first-timer concessions, or utilise HDB resale with Enhanced CPF Housing Grants for eligible upgrades without decoupling. Tenancy-in-common from purchase allows flexible share sales without initial severance.

Decoupling tax in Singapore is not a shortcut to avoid stamp duties, but a structured ownership strategy that must be applied carefully and genuinely. As ABSD rates remain high and unchanged through 2026, understanding the decoupling meaning, eligibility rules, costs, and long-term impact is essential before proceeding.

While decoupling property may help ensure homeowners manage ABSD exposure, it also involves BSD, legal fees, loan reassessments, and strict regulatory scrutiny. Under Decoupling Singapore, the outcome depends heavily on the buyer’s profile, property type, and compliance with IRAS and HDB rules.

Property owners should weigh tax savings against financial, legal, and future-planning considerations to decide whether decoupling is suitable or whether alternative ownership strategies offer a better fit.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.