Buying an HDB flat is a significant milestone, but managing the upfront costs can be challenging. For first-time buyers, understanding the BTO downpayment is crucial, as it represents the initial sum required when booking a new flat. To make things more manageable, the BTO staggered downpayment approach allows payments to be spread over time, reducing financial strain.

In 2025, HDB updated the staggered downpayment scheme 2025, offering lower initial payment percentages and more flexibility for young couples and first-time applicants. This guide explains how the scheme works, the eligibility criteria, and tips to plan your downpayment effectively.

Explore All HDB Resale Listings

Looking to buy an HDB flat?

How to Qualify for an HDB Flat (Video)

How Much Is HDB Downpayment?

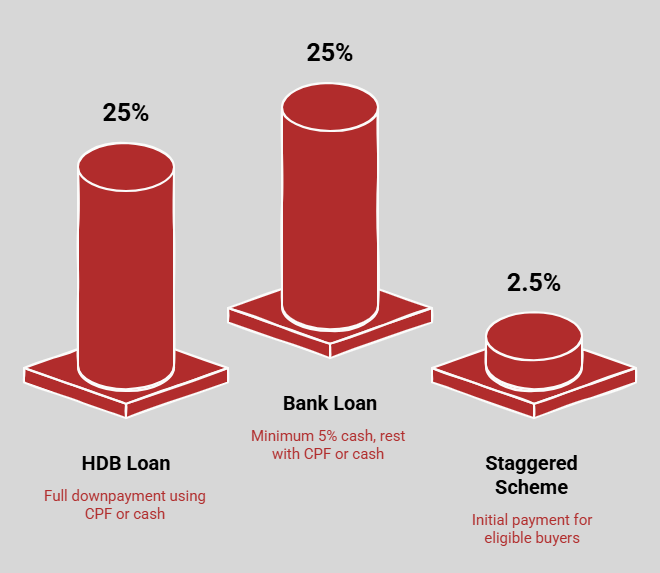

When purchasing an HDB flat in 2025, the downpayment is the portion of the flat price paid upfront before securing your home. Both HDB housing loans and bank loans now require a minimum downpayment of 25% of the flat price for BTO and resale flats. The actual breakdown depends on your loan type:

- HDB Loan: You can pay the full 25% downpayment using CPF Ordinary Account (OA) savings, cash, or a mix of both. This amount is usually split: 10% at the signing of the Agreement for Lease and 15% when collecting your keys, with a staggered scheme allowing payment at two stages (5% on lease signing and 20% upon key collection) for eligible buyers.

- Bank Loan: Minimum 5% of the flat price must be paid in cash. The remaining 20% can be paid with money, CPF OA savings, or a combination (for a total downpayment of 25%). You must obtain In-Principle Approval from the bank before disbursement.

- Staggered Downpayment Scheme: For eligible first-time buyers or young couples, the payment may be split into more miniature stages, with some cases allowing just a 2.5% initial payment, deferring the remainder to a later date.

This updated structure applies across BTO and resale flats, and you can use your CPF housing grants to offset part of the downpayment. Understanding these breakdowns is crucial for planning your budget and securing your home in Singapore.

Eligibility Criteria for the Staggered Downpayment Scheme

The Staggered Downpayment Scheme helps eligible flat buyers spread their downpayment into two instalments, making it easier to manage upfront costs. You don’t need to apply for this scheme separately; eligibility will be confirmed during your flat booking appointment.

Who Can Qualify

| Buyer Type | Eligibility Conditions |

| Couples | • Both applicants are first-timers, or one is a first-timer and the other a second-timer. • Applied for an HFE letter on or before the younger applicant’s 30th birthday. • Booked an uncompleted flat that is a five-room or smaller unit. |

| Existing Flat Owners (Right-sizing) | • Have not sold or completed the sale of their current flat at the time of applying for the HFE letter. • Booked an uncompleted three-room or smaller flat. |

This scheme mainly benefits younger couples buying their first home and existing homeowners looking to right-size, as it helps them manage their finances more comfortably while waiting for their new flat to be completed.

How Does the Staggered Downpayment Scheme Work?

The HDB Staggered Downpayment Scheme is designed to alleviate the financial burden of purchasing a new flat, particularly for young couples and first-time homeowners. Instead of paying the entire downpayment at one go, this scheme allows buyers to split the payment into two manageable stages. It is beneficial for those purchasing their flat early in life, when savings or CPF balances might still be limited.

Under the BTO Staggered Downpayment Scheme, the total downpayment is divided into two instalments:

- First Instalment: This portion is paid when you sign the Agreement for Lease, usually about nine months after booking your flat. By this time, you only need to pay a smaller share of the total downpayment, depending on your loan type (HDB or bank). The reduction in the initial payment helps ease cash flow during the early stages of your purchase.

- Second Instalment: The remaining portion is paid when you collect your keys, typically 2.5 to 4 years later, once construction is completed. This gives buyers a significant window to save up more money or build CPF Ordinary Account (OA) balances before making the final payment.

This system allows buyers to plan their finances effectively without depleting their savings upfront. For many young couples, the HDB Staggered Downpayment Scheme makes homeownership more achievable by matching payment timelines with their income growth.

Quick Loan Check

See if you qualify for a home loan as you explore your options.

Other HDB Downpayment Schemes

Apart from the HDB Staggered Downpayment Scheme, there are additional payment options designed to help specific groups of flat buyers manage their finances more comfortably. One such option is the Deferred Downpayment Scheme (DDS), which mainly benefits older homeowners who are planning to right-size their homes.

Deferred Downpayment Scheme (DDS)

The Deferred Downpayment Scheme allows eligible buyers, aged 55 and above, to delay paying the downpayment until they collect their flat keys. This is particularly useful for seniors who are selling their existing HDB flats to move into a smaller unit, as their funds might still be tied up in their current property.

Under this scheme, buyers only need to pay the stamp duty and legal fees when signing the Agreement for Lease, which usually happens within nine months after booking their new flat. The actual downpayment and purchase price are then paid later, at the point of key collection.

This delay gives seniors sufficient time to complete the sale of their existing property and free up their funds before making the payment.

To qualify for the DDS, applicants must:

- Be at least 55 years old at the time of the HDB Flat Eligibility (HFE) letter application.

- Have booked a two-room Flexi or three-room uncompleted HDB flat through any HDB sales exercise (either in a mature or non-mature estate).

- Not having sold or completed the sale of their existing HDB flat at the point of applying for the new one.

This scheme helps to smooth the right-sizing process by reducing immediate financial strain. It ensures that seniors do not have to pay two downpayments at once; one for their new flat and another while still holding onto their existing home.

The Deferred Downpayment Scheme complements the BTO Staggered Downpayment Scheme, offering flexibility to older homeowners in the same way the HDB Staggered Downpayment Scheme assists younger couples. Both initiatives share the goal of making homeownership and transitions between homes more financially manageable across different age groups.

Changes in Downpayment Percentages for 2025

The HDB Staggered Downpayment Scheme 2025 introduced several updates to make it easier for first-time homebuyers to manage their finances. These changes mainly focus on reducing the upfront payment and offering more flexibility in the payment schedule.

Here’s a breakdown of the key updates and what they mean for buyers:

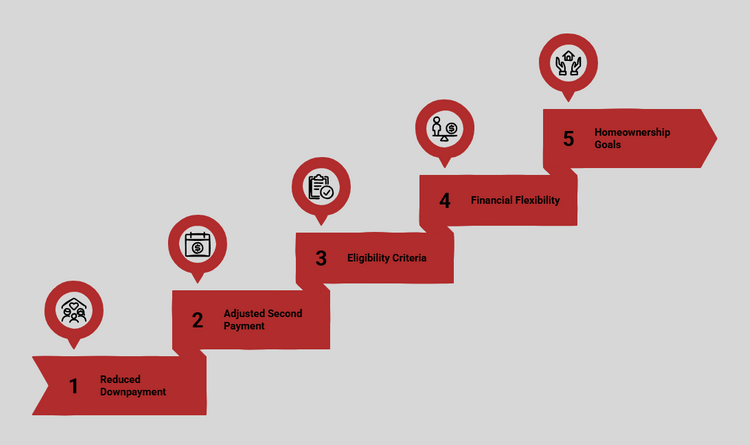

- Reduced Initial Downpayment (for eligible applicants)

- The first instalment at the Agreement for Lease stage can now be as low as 2.5% of the flat price, specifically for young couples or buyers who meet defined eligibility criteria, such as booking before age 30 or qualifying for Deferred Income Assessment.

- Most other buyers pay 5% at this stage.

- Adjusted Second Payment

- The remaining 22.5% (or higher, depending on loan type) is paid at key collection, 2 to 4 years later.

- This structure maintains the total 25% downpayment, giving buyers more time to save or accumulate CPF OA funds.

- Eligibility

- Key conditions include being a first-timer, applying before the younger applicant’s 30th birthday, or qualifying for Deferred Income Assessment.

- The scheme applies only to uncompleted flats (BTO, Sale of Balance, Open Booking).

- Financial Flexibility and Homeownership Goals

- Buyers benefit from improved cash flow management at signing and more time before the main payment.

- The changes support affordability and early homeownership for qualifying groups, in line with HDB policy aims.

- Alignment with HDB’s Affordability Goals

- These adjustments align with HDB’s broader mission to enhance housing affordability.

- By easing upfront costs, the HDB staggered downpayment scheme ensures that homeownership remains achievable and sustainable across different income levels.

These adjustments improve financial flexibility while supporting HDB’s ongoing commitment to making homeownership more accessible and affordable.

How Does the Staggered Downpayment Scheme Benefit First-Time Buyers?

The HDB Staggered Downpayment Scheme provides a flexible payment structure that greatly helps first-time homebuyers manage their financial commitments more comfortably. Instead of paying the entire downpayment upfront, buyers can split it into two smaller payments, one when signing the lease and the other when collecting the keys. This approach offers several practical advantages:

1. Provides Financial Breathing Room

- Many first-time buyers are young couples who have just started working and may not have significant savings.

- Under the BTO Staggered Downpayment Scheme 2025, young couples applying under the Fiance/Fiancee Scheme or other eligible first-time buyers only need to pay a smaller upfront amount of (2.5% for HDB loans) when signing the Agreement for Lease, instead of the previous 5% to 10% requirement.

- This allows them to secure a flat earlier without feeling overwhelmed by a large initial expense.

2. Reduces the Pressure to Use All Savings Immediately

- Traditionally, buyers had to prepare a large lump sum at the lease signing stage.

- The staggered payment structure reduces the need to empty personal savings or fully depend on CPF Ordinary Account (OA) balances.

- This means buyers can retain funds for emergencies, wedding expenses, or furniture purchases while still moving forward with their home purchase.

3. Encourages Better Financial Planning

- The gap between the two payments gives buyers two to four years (until key collection) to plan their finances.

- They can save progressively, top up their CPF OA, or adjust their spending habits to prepare for the second instalment.

- This promotes responsible money management and ensures buyers are financially ready when their new home is completed.

4. Lowers Overall Financial Stress

- By spreading payments over time, the HDB staggered downpayment scheme reduces the emotional and financial strain often associated with large purchases.

- Buyers can focus on career growth or starting a family instead of worrying about immediate financial burdens.

- This structure also lessens the need for personal loans or borrowing from family, which further eases long-term stress.

5. Makes Homeownership More Accessible

- The staggered approach allows first-time buyers to enter the property market earlier, even if they haven’t saved a huge amount yet.

- It also ensures that homeownership remains within reach for middle-income families, aligning with HDB’s aim of maintaining affordability and inclusivity.

The Staggered Downpayment Scheme makes homeownership more achievable and less stressful for first-time buyers. By splitting payments over time it provides financial breathing room, encourages better planning, and ensures that young couples and eligible buyers can move into their flats without feeling overwhelmed by upfront costs.

How Can You Manage Your HDB Downpayment Efficiently?

Managing your HDB downpayment wisely plays a crucial role in ensuring a smooth and stress-free homebuying experience. With the HDB staggered downpayment scheme and other support measures, buyers can plan their finances strategically without feeling overwhelmed.

Here are some effective ways to handle your BTO staggered downpayment efficiently:

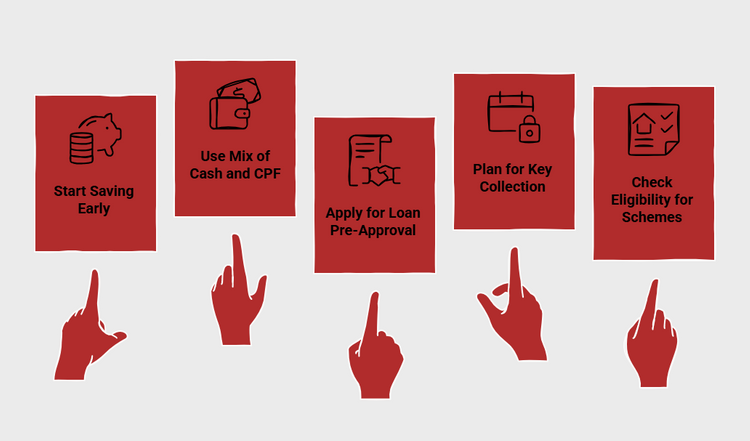

1. Start Saving Early and Track Your CPF OA Balances

- Begin setting aside a fixed portion of your income the moment you decide to buy a flat.

- Regularly monitor your CPF Ordinary Account (OA) balance, as it directly contributes to your downpayment.

- Starting to save early helps young couples and first-time buyers comfortably cover the initial 2.5% payment under the Staggered Downpayment Scheme 2025 without depleting their cash reserves.

- CPF’s online tools can help you estimate how much you’ll accumulate by the time your flat is ready.

2. Use a Mix of Cash and CPF OA for Better Flexibility

- While CPF savings can cover most of your downpayment, it’s wise to maintain a balance between cash and CPF OA.

- Paying partly in cash ensures that you don’t completely deplete your CPF savings, which continue earning interest.

- This mix provides greater control over your finances, especially when other significant expenses, such as renovation or furnishing, arise after key collections.

3. Apply for Bank Loan Pre-Approval (IPA) Early

- If you’re planning to take a bank loan instead of an HDB loan, always get an In-Principle Approval (IPA) before booking a flat.

- This step helps you understand your loan eligibility, interest rates, and downpayment amount clearly.

- Having an IPA in hand ensures there are no unpleasant surprises or delays during the Agreement for Lease stage.

- It also makes financial planning easier since you’ll know exactly how much to set aside for the first and second downpayment portions.

Estimate Your HDB Loan Instantly

Planning to buy an HDB flat?

4. Plan for Key Collection Payment Well in Advance

- The second part of the staggered downpayment is usually due when you collect your keys, which can be two to four years after booking your flat.

- To prepare, estimate your future cash flow and project how much you’ll have saved by then.

- Set up a monthly savings goal dedicated to this payment, using either automatic transfers to your CPF OA or a separate savings account.

- This proactive approach prevents last-minute financial stress and ensures that you’re ready when the project is completed.

5. Check Your Eligibility for Payment Assistance Schemes

- Review if you qualify for schemes like the Deferred Downpayment Scheme (DDS) or the HDB staggered downpayment scheme, as they are designed to ease upfront financial strain.

- The DDS, for example, allows elderly homeowners or those right-sizing their flats to defer payments until key collection.

- These government-backed options can significantly reduce initial costs, making homeownership more accessible to various income groups.

The 2025 HDB Staggered Downpayment Scheme offers first-time buyers a more flexible and manageable way to fund their homes, making early homeownership less financially daunting. With this scheme, buyers can plan their finances better while securing their flats with smaller upfront payments.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.