The condo payment schedule Singapore for 2025 provides a structured outline of when and how a property buyer must make payments during the purchase of a condominium, especially for new or under-construction projects.

Instead of paying the full amount upfront, the system spreads payments over several stages. Each stage corresponds to specific construction or legal milestones, which allows buyers to manage their finances more efficiently.

The Progressive Payment Scheme (PPS) is the key framework governing these instalments. It ensures that buyers pay only when the development reaches certain stages of completion, such as the foundation, framework, or finishing. This helps both developers and buyers maintain transparency and balance financial obligations throughout the building period.

Applicability of the Schedule to New and Under-Construction Projects

The payment schedule primarily applies to new launch condominiums and under-construction developments, also referred to as Buildings Under Construction (BUC). These projects follow the PPS, which spreads payments across construction milestones.

For completed or resale condos, the structure is quite different. Resale condo payment schedules are usually made in a few lump sums: a downpayment upon exercising the Option to Purchase (OTP), and the remaining amount upon completion.

The PPS, first introduced to regulate payments for new developments, ensures buyers pay in line with verified progress reports, thereby reducing the risks associated with incomplete projects.

Start your home search with ease.

Check out available HDB flats for sale.

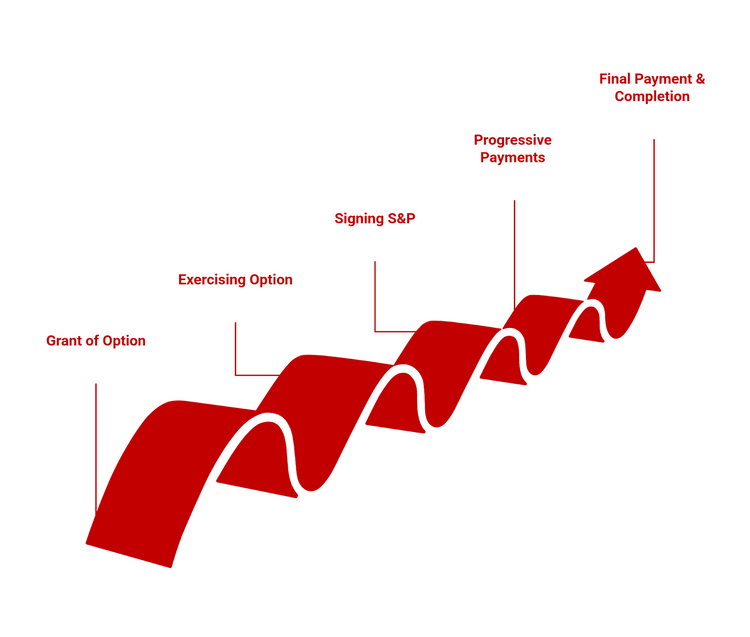

What are the Key Stages in the Condo Payment Process?

The condo payment process unfolds in a series of clear steps, starting from securing a unit to completing the final legal requirements. Each stage involves specific fees, documents, and timelines that guide buyers from the initial booking to full ownership.

- Grant of Option to Purchase (Booking Fee)

The process begins when a buyer chooses a unit and pays a booking fee, typically 1% of the purchase price, in cash. This payment secures the chosen unit temporarily and grants the buyer an Option to Purchase (OTP), giving exclusive rights to proceed with the purchase within a set timeframe (usually 14 days).

- Exercising the Option to Purchase (Option Fee)

To confirm the purchase, the buyer must use the OTP within 14 days and pay an additional 4% of the purchase price, also in cash. This brings the total initial commitment to 5%. Failing to exercise the OTP within the timeframe may result in forfeiture of the booking fee and release of the unit back to the developer.

- Signing the Sale and Purchase Agreement (S&P)

Once the OTP is exercised, the Sale and Purchase Agreement (S&P) is prepared and signed, typically within three weeks. This legal document outlines the terms of the sale and officially binds both parties to the transaction. After signing the S&P, the buyer must pay the Buyer’s Stamp Duty (BSD) within 14 days.

- Progressive Payment for Condo Based on Construction Milestones

After the initial downpayment, the remaining purchase price is paid in instalments as the development reaches construction milestones: foundation, framework, walls, roofing, and finishing. These payments, typically financed through a bank loan, are disbursed in accordance with the developer’s progress certification.

- Final Payment and Legal Completion

The final payments are made upon legal completion, typically upon issuance of the Temporary Occupation Permit (TOP) and subsequently the Certificate of Statutory Completion (CSC). These milestones mark the developer’s fulfilment of building obligations and the buyer’s complete ownership transfer.

Understanding the Progressive Payment Scheme (PPS)

The Progressive Payment Scheme outlines how buyers pay for a property in stages rather than in a single lump sum. It breaks the total cost into manageable instalments for each construction phase, helping buyers plan their finances with greater clarity.

How PPS Works

The Progressive Payment Scheme (PPS) divides the total property price into instalments, aligning payments with construction progress. Instead of paying in one lump sum, buyers pay smaller percentages each time the developer reaches a certified milestone. This system lightens the immediate financial burden and aligns payment obligations with the project’s physical progress.

Typical Payment Percentages by Construction Stage

The payment structure typically follows this order:

- Foundation – around 15%

- Reinforced concrete framework – around 20%

- Brick walls and plastering – around 5% each

- Fixtures, fittings, doors, and windows – about 20% across several sub-stages

- Temporary Occupation Permit (TOP) / CSC – approximately 15%

- Legal completion – about 15%

Note: Payment percentages by construction stage vary significantly depending on the specific project, contract terms, location, and changes that occur during construction.

Timeframes for Each Payment Stage

For each milestone, the developer issues a formal notice of completion. Buyers must make their payments within 14 days from the date of notice. Failing to pay within this timeframe may attract interest charges or penalties as outlined in the S&P.

Detailed Breakdown of Payment Stages for New Launch Condos

Buying a new launch condo involves a structured payment sequence that begins with securing the unit and continues through construction and final handover. Each stage has its own payment requirement, helping buyers plan their finances as the project moves from launch to completion.

- Booking Fee and Initial Option Payment

The initial 1% booking fee secures the unit, followed by a 4% option exercise payment within 14 days. This ensures the developer reserves the property and proceeds to the following legal steps once the buyer commits.

- Downpayment Structure (Cash vs CPF)

After the option is exercised, buyers pay a 15% downpayment, generally within eight weeks. Of this amount, 5% must be paid in cash, while the remaining 10% may be paid from CPF savings or additional cash.

- Construction-Linked Instalments

As construction progresses, payments are released in stages: foundation, framework, wall construction, and internal finishing. Banks typically coordinate with the developer to release these funds once the milestones have been verified.

- Payment on Certificate of Statutory Completion (CSC) and TOP

Upon obtaining the TOP, a significant 25% payment is required. The final 15% is due upon legal completion. At this point, buyers can take full possession and begin occupying the property.

Note: Exact percentages and timing may vary based on developer, project, contract terms, and regulatory requirements.

Your next home or investment awaits.

Discover properties for sale across Singapore.

Downpayment Requirements for Condominiums

Buying a condominium requires careful planning, especially when it comes to the upfront downpayment. This section explains the key downpayment requirements so you know exactly what to prepare before making your purchase.

- Minimum Cash Downpayment Required

All buyers must pay at least 5% of the property price in cash, as this cannot be covered by CPF or bank financing. It is the mandatory upfront commitment required to secure the unit.

- Use of CPF for Downpayment

After fulfilling the cash requirement, buyers can use their CPF Ordinary Account (OA) funds for part of the downpayment or subsequent progressive payments, subject to CPF limits and eligibility.

Looking for modern living with great amenities?

Explore condominiums available for sale.

Differences Between New Launch and Resale Condominium

Price (psf)

Higher, often above S$2,200 psf (up to S$3,000+ in prime areas)

Generally lower, around S$1,500 to 1,700 psf

Initial payment structure

Progressive Payment Scheme: booking fee, option fee, downpayment, then staged payments linked to construction

Lump sum payments upon exercise of the option and completion

Downpayment

Typically 15%, with at least 5% in cash upfront, the rest can be CPF or cash

A full downpayment is usually required at the time of purchase

Payment schedule

Staggered progressive payments tied to construction milestones

Full payment and loan disbursement are typically made at purchase completion

Loan disbursement

Progressive loan disbursement aligned with the payment schedule

Full loan disbursed immediately upon transaction completion

Maintenance costs

Low initially, as units and facilities are brand new

Higher, as older developments may require more upkeep or renovations

Renovation

Minimal to none, as units come brand new with fittings

Often needed, which adds to the initial upfront cost

Rental income

No rental income during the construction period (usually years)

Immediate rental income possible as units are move-in ready

Capital appreciation potential

Higher, especially if bought at launch price and sold post-TOP

Typically lower but more stable, may depend on market conditions

Move-in timeline

Waiting period of several years till project completion

Immediate or short-term move-in possible

Location/environment

Newer developments, often in growing or developing areas with modern designs

More established estates with mature amenities

Buyer considerations

Suitable for buyers prioritising modernity, future capital gains, and the latest facilities

Ideal for buyers seeking immediate returns, larger layouts, and established communities

This comparison shows that new launch condos involve more staggered payments tied to construction progress, offering more payment flexibility but requiring more financial planning.

Resale condos require larger upfront cash outlays but offer quicker occupancy and potential rental income. The choice depends on buyers’ financial capabilities, timing preferences, and investment goals.

Payment Methods: Cash, CPF, and Bank Loans

In most purchases, payments are made through a combination of cash, CPF savings, and bank loans.

- Cash is required for the initial booking fee and part of the downpayment.

- CPF funds can be used after the mandatory cash portion.

- Bank loans cover the remaining purchase amount and are disbursed progressively as the developer issues completion certificates.

Buyers must synchronise bank disbursements and CPF usage to avoid late payment issues.

Buyer’s Stamp Duty and Other Legal Fees

The Buyer’s Stamp Duty (BSD) must be paid within 14 days of signing the S&P. The BSD rates are progressive, as follows:

- 1% on the first S$180,000

- 2% on the next S$180,000

- 3% on the next S$640,000

- 4% on the remaining amount

For high-value properties or multiple property ownership, Additional Buyer’s Stamp Duty (ABSD) may also apply.

Legal Fees and Valuation Fees Breakdown

- Legal fees: Typically between S$2,500 and S$4,000, depending on the property price and complexity.

- Valuation fees: Usually range from S$350 to S$500 and are required when applying for a bank loan.

These costs should be factored into your overall budget and paid early during the legal process.

Calculate your stamp duty quickly and accurately.

Use our stamp duty calculator today.

Payment Schedule for Executive Condominiums (ECs) in 2025

Understanding how EC payments are structured in 2025 helps buyers plan with confidence. Although ECs follow the progressive payment flow used in private condos, they also come with additional HDB guidelines, making their payment process slightly different. This section outlines what buyers can expect when paying for an EC this year.

Differences in Payment Terms Compared to Private Condos

While ECs follow the same general condo progressive payment timeline framework as private condos, they are subject to Housing and Development Board (HDB) regulations. EC buyers can choose between two schemes:

- Normal Payment Scheme (NPS): Similar to PPS, where payments are made progressively.

- Deferred Payment Scheme (DPS): A larger portion of the payment is postponed until the project receives the TOP, offering more time to manage finances.

Minimum Upfront Payment and Loan Conditions

EC buyers must make a minimum 5% cash downpayment, with the rest payable through CPF or bank loans. However, loan eligibility and limits are determined by the Mortgage Servicing Ratio (MSR) and HDB guidelines, which are stricter than those for private property purchases.

Tips to Manage Your Condo Payment Timeline Efficiently

Managing your payment timeline well ensures a smooth buying experience from the day you book your unit until the final handover. A little planning can help you avoid penalties, stay organised, and keep your finances stable throughout each milestone. Here’s how you can stay in control of every stage.

Ensuring Timely Payments to Avoid Penalties

Always make payments within the stipulated 14-day period after receiving notice from the developer. Late payments can result in penalty interest or even cancellation of your purchase rights. Setting up reminders or automatic transfers from your loan or CPF accounts can help you stay on schedule.

Effective Use of CPF and Cash Savings

Strategically plan how much CPF and cash to allocate for each payment stage. Maintain cash reserves for emergencies, and ensure that your CPF balance covers upcoming milestones. Always keep your loan-to-value ratio and monthly instalment capacity in check to stay financially stable.

Consequences of Late Payments and Penalty Charges

Late payments can affect both your purchase rights and your financial commitments, so it’s essential to understand the risks involved. This section explains the penalties, interest charges, and project delays that may arise when payments are not made on time, helping you stay prepared and avoid unnecessary setbacks.

Penalties for Late Payments to the Developer

Payment delays often attract penalty interest, typically 5% above the prevailing bank rate, as stipulated in the Standard & Poor’s (S&P) guidelines. Continuous non-payment can lead to cancellation of the sale and the forfeiture of any prior payments.

Impact on Loan Disbursements

Late payments may also delay bank loan disbursements, creating a domino effect that disrupts your payment schedule and could result in financial strain. Timely communication with your bank and solicitor is crucial to prevent such issues.

Are There Any Changes in 2025 Compared to Previous Years?

The core structure of the Progressive Payment Scheme timeline remains unchanged in 2025. However, regulatory updates, bank loan criteria, and CPF usage limits may vary slightly. Buyers should verify these details before making a purchase commitment.

Table: Example Progressive Payment Breakdown (New Launch Condo)

The table below gives a quick snapshot of how payments are typically spread out for a new launch condo.

Booking Fee (Option Grant)

On Booking

1%

Cash

Exercise Option

Within 14 days of booking

4%

Cash

Downpayment

Within eight weeks of the option

15%

Cash/CPF

Foundation Stage

Six to nine months after launch

10%

Cash/Loan

Framework Completion

Six to nine months later

10%

Cash/Loan

Brick Walls & Ceiling

Three to six months after the framework

10% (across stages)

Cash/Loan

TOP/CSC Stage

Upon certificate issuance

25%

Cash/Loan

Legal Completion

At legal completion

15%

Cash/Loan

This breakdown offers a general idea of the payment flow, but actual timelines and percentages may vary slightly depending on the developer and loan arrangement. Buyers should always check the final schedule in their Sale and Purchase Agreement for the exact details.

How Does the 2025 Condo Payment Schedule Guide a Smooth Buying Experience?

The 2025 condo payment schedule in Singapore continues to provide a structured and secure approach for property purchases. Understanding each stage, planning your finances, and tracking timelines are key to a smooth, successful condo ownership journey.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.