The HDB market is seeing some signs of optimism, but it’s too early to call it a recovery. Where will the market head to in 2016? We give you the Guru View.

By Adam Rahman and Chang Hui Chew

While condo transactions continue to be scrutinized by most market watchers, often due to the aspirational nature of the property class, it is necessary to keep an eye on HDB resales. To Singaporeans, HDB has always been a very bread and butter issue, with a large majority of families living in them.

Furthermore, for those looking to upgrade from public housing, they would need to sell their HDB starter homes, hopefully with a decent upside, to be able to afford the move to condominiums, or executive condominiums (ECs). The health of the HDB resale market, therefore, affects the private market as well.

We take a closer look at the ups and downs of the HDB market in 2015 to make some predictions for where this market segment will head in 2016.

Overall HDB market

What then, was the pulse of the HDB market in 2015?

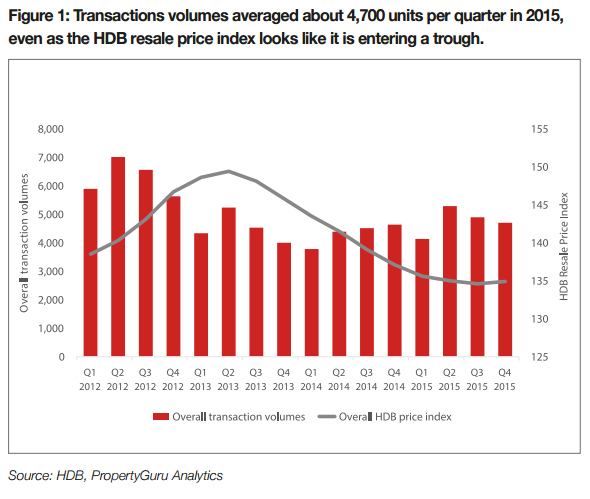

In the space of the 12 months of 2015, 19,015 HDB resale units exchanged hands, a 10 percent increase from 2014’s 17,318 (refer to Figure 1). This translates to an average of around 4,700 units transacted per quarter of the year, with the second quarter seeing a high of 5,286 units. This is comparable to the numbers that were seen in 2012 and 2013, before cooling measures froze the market and reduced transactions to a mere trickle.

While the number of transactions increased, prices dipped 1.6 percent. This decline is a far milder than the 6.1 percent dip seen in 2014, suggesting that the fall in prices might be coming to a trough. A burgeoning sign of promise was that prices actually saw a small 0.2 percent bump in the final quarter of the year, according to the HDB resale price index. However, most market watchers caution that it is far too early to call it the start of a recovery, and that more sustained signs of recovery must be seen.

The two key cooling measures that have brought about this fall in prices in the HDB resale market are the Mortgage Servicing Ratio (MSR), and the removal of Cash-Over-Valuation (COV). MSR caps the payable monthly mortgage 30 percent of one’s monthly income. Buyers therefore have to look at what the bank tells them they can afford, instead of what they think they can afford.

The removal of COV was a welcome move as well, because sellers often focused on COV to determine their asking price. This meant that buyers were paying more than the fair valuation price, and had to pay premiums to buy a unit. Furthermore, sellers often set higher and higher COVs, based on what they heard their neighbours had sold for, creating a system of escalating quantums. Removing COV, therefore, put some sense back into the system.

It might be better therefore, to see where HDB prices have gone, not so much as a downturn, but rather, as some kind of sensibility entering the market, with sellers making more rational decisions around the pricing and the actual value of their homes.

Breaking down the numbers

Despite prices falling across the board, the picture gets more complex once we delve into the details.

In general, flats in mature housing estates have held up better in terms of prices than their non-mature counterparts. For instance, the top five performing estates in terms of median prices for four-room flats were Serangoon, Bukit Merah, Geylang, Kallang / Whampoa, and Queenstown. Geylang’s prices showed a 15.3 percent increment, an incredible jump, given the market. However, due to the relatively small size of the estate, it did not move the overall market needle.

Meanwhile, the top five performing estates for five-room flats were also mature estates. Geylang again took the crown, with Toa Payoh, Ang Mo Kio, Bishan and Yishun coming in below it, all showing more moderate increases below two percent.

With the distribution and buildup of resources across the island, it is likely that the reason mature estates do better is due to the greater number of amenities available. Rather, all the mature estates that performed well in 2015 were located within a 20-minute MRT ride to the city, or even closer. Furthermore, Bukit Merah, Queenstown and Kallang / Whampoa are receiving a lot of attention from affluent, younger couples who are drawn to the revivification of those estates with hipster cafés, bars and shops.

Supply is likely to play a part as well. Aside from Ang Mo Kio and Toa Payoh, these are all smaller, early estates. The supply of resale flats within these areas is unlikely to be high, and many of the older blocks could have already been earmarked for HDB’s Selective Enbloc Redevelopment Scheme (SERS), which would discourage people from buying them, only to face the hassle of relocation in the future. This lowered supply then, continues to support elevated prices.

Record busters

In 2015, 110 HDB units sold for prices above $900,000.

Out of these, 53 were units at Pinnacle at Duxton, where record prices continue to be set for HDB flats. In fact, the highest price ever recorded for a four-room flat took place at Pinnacle at Duxton this year, for $990,000. However, even though over 50 units were sold for above $900,000, only nine managed to cross the psychological one million dollar mark, all of which were five-room units.

Three other flats sold in 2015 also managed to cross this threshold. These flats were located in Toa Payoh, Toh Yi Drive and Jalan Ma’mor. The Jalan Ma’mor flat is particularly interesting, because it is also a rare jumbo unit at 3,014 square feet, and sold for $1,060,000. Its size, rarity and location close to Balestier and Novena were factors that contributed to its higher prices.

While we are all used to Bishan’s million dollar maisonettes, it might be surprising to some that Toh Yi Drive also saw seven duplex units move at prices over $900,000, with one unit going for a million on the dot. The proximity to the Bukit Timah school stretch, and the newly opened Beauty World MRT on the Downtown Line likely contributed to those prices. Marine Parade also saw three flats that went for over $900,000. All three were located in point blocks, within walking distance to the beach, and also to the ever-popular Tao Nan School.

These unit types – jumbo flats, point blocks and executive maisonettes – are no longer built, which has definitely made them scarcer. For those looking to live in such units, therefore, and want the conveniences of amenities, popular schools and transport links, there is definitely a premium price to be paid.

Market insiders revealed that buyers of these record breaking flats were unlikely to be regular HDB upgraders. Often, these were owners of private property, who had cashed out of their homes with really decent capital appreciation, and were willing to pay top dollar to purchase a home in a location they desired. They are therefore the exception, rather than the rule.

Public rentals

On the surface, the HDB rental market looks like it is doing quite well. The number of transactions in 2015 was 13 percent more than 2014’s, with 41,109 rental contracts reported to HDB. Five-room units are the most popular, with a 22 percent increase year-on-year (refer to Figure 2).

The pricing story, however, is a lot more depressing for landlords and homeowners. Overall, the year saw a four percent dip in median prices from 2014. Some of the sharpest drops year-on-year came from popular locations. For instance, Marine Parade saw median four-room rental prices drop by a rather steep 11 percent, while Bukit Merah saw prices for the same sub-type decline seven percent.

As such, those who have suggested that the HDB rental market is recovering have actually called it in error. In places like Marine Parade, for instance, tenants could easily threaten to move to a rental condo instead of sticking with a HDB, because declines have also brought down rents in the private market. Most landlords would rather capitulate than lose a tenant and have the unit sit empty.

The reason for the higher number of rental contracts signed is not because tenants have increased. Rather, it is because the frequency of contracts being signed have increased, because tenants are opting for one- instead of two-year contracts, negotiating for further concessions from landlords, be it rental price reductions, new furniture, or subsidized utilities.

Ball gazing

So where is the market likely to move in the next 12 months?

For HDB resale transactions, our house view is that transactions will gain further momentum, even as prices continue to fall. With a bumper crop of 28,000 new Build-to-Order (BTO) flat owners receiving their keys this year, we will likely see an increase in resale flats hitting the market, as upgraders will need to move their existing units within six months. We think that sales volume is likely going to be between 4,200 and 5,400 per quarter, with 2016 closing with under 20,000 units exchanging hands. Given seasonal fluctuations, resale prices are likely to vary about 1.5 percent up or down each quarter. We think that the year is likely to end with overall prices falling between 0.3 and 0.8 percent.

The prognosis of the rental market is more dismal. While volumes might climb moderately, we are likely to see a sharper decline in prices. With a projected global economic slowdown, as well as the political climate on foreign labour remaining negative, there are fewer demand drivers for the rental market.

With a bumper crop of over 50,000 dwelling units hitting the market, there will be a supply glut in the market. HDB rentals are likely going to find themselves competing with investment units in suburban condos, as they race to the bottom dollar to find tenants.

Furthermore, those upgrading from HDBs to condominiums might decide to hold on to their flats and rent them out for income while waiting for prices to further appreciate, exacerbating the supply issue. As such, our house view is that rental prices for HDBs are going decline further by five to eight percent.

| This article was first published in the print version PropertyGuru News & Views. Download PDFs of full print issues or read more stories now! |

|||