There is no shortage of housing rules and regulations in Singapore. Understandably, the ins and outs of home loans can seem complicated and confusing, so we have put together a quick but essential guide to loans from the HDB and from banks, to help you decide if you should switch from former to the latter.

If you are a Singaporean who bought your first HDB flat 10 years ago, you would have taken up a HDB concessionary loan. The odds are that you were a newlywed twenty-something earning less than $5,000 a month, with your spouse in a similar income bracket.

Now, 10 years later, you both enjoy higher salaries, and the HDB market is currently experiencing low-interest environment. As such, you may be tempted to refinance your mortgage with a bank or financial institution, in order to benefit from better savings.

At PropertyGuru’s Mortgage Marketplace, you can find all the information you need regarding mortgages: from mortgage calculators to guides, as well as a wide selection of mortgage loans from over 14 major banks, it is now easier to choose a refinancing package that best meets your needs.

The HDB’s interest rate has remained the same for the last 10 years

Most people who take up a HDB loan choose it for the stable interest rate. Pegged at 0.1 percent above the prevailing CPF interest rate, it has held constant at 2.60 percent per annum.

This gives homeowners greater peace of mind, since they do not have to worry about fluctuating interest rates affecting their monthly mortgage payment. If there are young children and elderly parents in your family, you will certainly appreciate the stability that comes with a HDB loan.

However, the drawback is that HDB interest tends to lag behind market developments. If interest rates drop significantly — as they did last year, to historically low levels — you could end up paying more than if you had taken up a bank loan.

Once you accept a bank loan, you cannot revert to a HDB loan

This sounds almost ominous, but bear in mind that you are not permitted to switch back to a HDB loan after you refinance your loan with a bank. Once you take up a bank loan, you are basically on your own.

As such, before you commit to anything, it might be a good idea to consider all the housing loan packages offered by major banks at Mortgage Marketplace, then weigh the pros and cons of each package.

The HDB is likely to be more sympathetic should you default on your home loan

As Singapore’s public housing authority, as well as a statutory board under the Ministry of National Development (MND), the HDB tends to show greater leniency to homeowners who fall on hard times and as a result, default on their home loan. For genuine cases, the HDB is unlikely to foreclose on a property.

Although the bank loan officer overseeing your case may want to help you as best he can, most banks are still privately owned businesses whose management has to ensure they cut their losses. As a financial institution, a bank will try to recover any bad debt, and is therefore unlikely to be able to show the same leniency the HDB tends to show to defaulters.

Unlike banks, the HDB does not impose an early repayment penalty

If you can somehow repay the remainder of your home loan early, the HDB will accept this early repayment with no questions asked. On the other hand, if you try to repay your bank loan fully before the loan term is up, you will have to also pay a 1.5 percent pre-payment penalty.

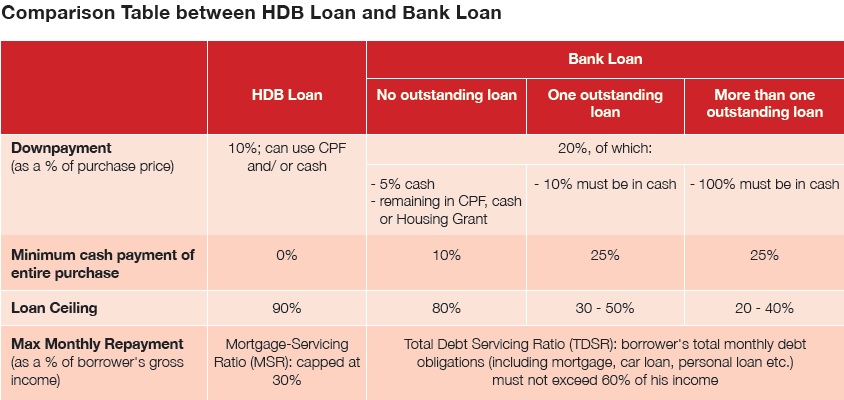

At the same time, compared to a bank loan, a HDB loan requires a lower or even zero cash outlay; for more detailed information, simply refer to the table on the next page for a side-by-side comparison.

HDB loan customers have greater access to CPF savings

While bank loan customers are required to pay at least five percent of their 20 percent deposit in cash, HDB customers can use CPF savings for their entire 10 percent deposit.

For repayments on new flats, HDB loan customers have unlimited access to their Ordinary Account. As for resale flats, they can withdraw up to the Valuation Limit of the flat, and in some cases an additional 20 percent beyond this, provided they meet minimum sum requirements.

Choosing a bank loan

To help ease your cash flow, banks offer a variety of repayment choices. The three most common types are fixed-rate loans, variable interest loans, and loans with interest rates pegged to the Singapore Interbank Offered Rate (SIBOR).

Let’s take a more detailed look at each type of loan:

• Fixed-Rate Loan: With a fixed-rate loan, your monthly instalment is locked for an agreed period of time, usually for the first one or two years of your loan, to protect you from rate fluctuations. At the end of the fixed-rate period, the interest rates will be based on the bank’s board rate, i.e., rates set internally by the bank. Some banks offer a discount on the board rate, so do not hesitate to ask about or negotiate for a better rate.

• Variable Interest Rate Loan: For loans with variable interest rates, you can expect to pay lower interest. However, the interest tends to fluctuate with the bank’s board rate, so there is a degree of uncertainty regarding how much you can expect to pay. There is also a lock-in period, usually one to three years, to discourage you from refinancing your loan during that time. Should you switch banks before the lock-in period is over, you will be subject to a penalty fee.

• SIBOR-dependent Loan: The interest rates for this type of loan are pegged to the SIBOR. The SIBOR is reviewed every three months, and has varied between 0.6 and 3.5 percent in the last five years. For their offered rate, banks usually add on a fixed percent age to the SIBOR. Due to the current low SIBOR, this type of loan probably offers you the lowest mortgage payment every month. Just be mindful that your mortgage is likely to increase if the SIBOR rises significantly.

Conclusion

By refinancing your HDB concessionary loan with a bank loan, you could benefit from prevailing low interest rates and save a few hundred dollars every month. While a HDB loan is the standout choice if you value stability, there are smart savings to be made in the short- to medium-term if you opt for a bank loan.

For someone struggling to make the initial down payment using cash, a HDB loan is the way to go. Just bear in mind you are paying a premium (about one percent, the difference between the interest rate on a HDB loan and bank loan) for this convenience. You may also wish to revisit your financing options years down the road, to benefit from possible savings.

It is important to note, however, that if you choose to take up a bank loan rather than a HDB loan, this is irreversible. You cannot revert your loan to a HDB loan, or take up a new HDB loan after that.

For the best selection of home loan packages in Singapore, visit PropertyGuru’s Mortgage Marketplace at: www.PropertyGuru.com.sg/mortgage

Disclaimer: Information provided in this publication is general in nature and does not constitute professional financial advice. PropertyGuru will endeavour to update its publication and website as needed. However, information can change without notice, and we do not guarantee the accuracy of information in the publication or on the website, including information provided by third parties, at any particular time.

Whilst every effort has been made to ensure that the information provided is accurate, individuals must not rely on this information to make a financial or investment decision.

Before making any decision, we recommend you consult a financial planner or your bank to take into account your particular financial situation and individual needs.

PropertyGuru does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this publication or on its website.

Except insofar as any liability under statute cannot be excluded, PropertyGuru and its employees do not accept any liability for any error or omission in this publication or on its website or for any resulting loss or damage suffered by the recipient or any other person.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||