Singaporean homeowners have faced relentless pressure on their household budgets over the last few years. From the rising cost of daily groceries to higher utility tariffs, managing family cash flow requires careful and constant planning. When the annual property tax notices arrive in the mail, many families naturally brace themselves for a financial hit. The system calculates property tax based on the estimated rental value of your flat, and those rental values have climbed significantly across the island following the recent housing boom.

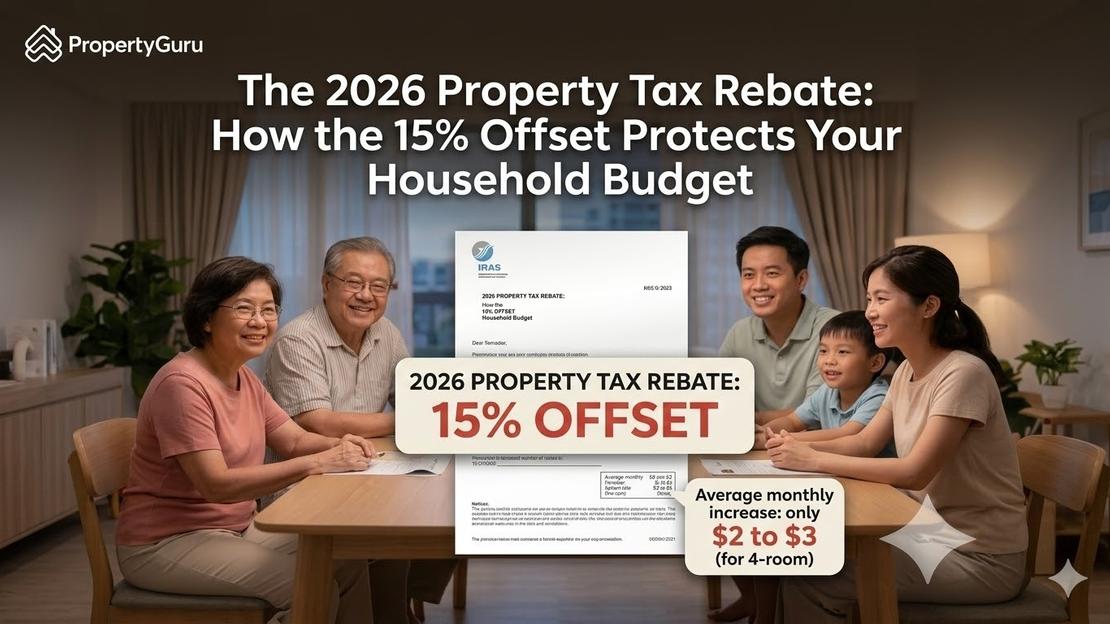

However, the government has recognised this exact pressure and deployed a targeted financial cushion to protect public housing owners from sudden payment shocks. By stepping in to absorb a portion of the tax hike, the authorities are ensuring that basic homeownership remains affordable for the average citizen. Announced in late 2025 and effective for the 2026 tax year, a one-off 15% property tax rebate for owner-occupied HDB flats is automatically applied to tax statements. This intervention cushions the 2026 rate hike, keeping the average monthly increase for 4-room owners to just $2 to $3.

Why is the government stepping in to lower your tax bill?

To understand why you are getting a 15% rebate, you first need to understand how the Inland Revenue Authority of Singapore (IRAS) calculates your property tax. The government does not tax your flat based on how much you bought it for. Instead, they use a system called the Annual Value (AV). The AV is the estimated amount of money you could collect if you rented out your entire flat to tenants for a full year. Even if you live in your flat and have no intention of renting it out, the government still calculates this theoretical rental income. They then charge a small tax percentage on that theoretical amount.

Over the last few years, the rental market in Singapore became expensive. Because real-world rental prices went up aggressively, the theoretical AV of HDB flats also increased. When your flat AV increases, your property tax bill automatically increases with it. The government recognised that it can be frustrating to hit an owner-occupier with a tax bill just because the rental market is running hot. To fix this, the Ministry of Finance introduced this one-off 15% rebate. This rebate acts as a direct shield, intercepting the tax increase before it hits your bank account and softening the blow.

How much money does this actually save you?

Translating these tax formulas into plain English reveals exactly how much cash the government is helping you retain. Without this government intervention, rising AVs would have caused a noticeable spike in yearly expenses. A standard four-room HDB flat might have seen its property tax jump by $50 to $80 for the year.

Because IRAS automatically applies the 15% discount to your final bill, that sharp spike is significantly reduced. Instead of a large jump, the average four-room flat owner will only see their total yearly bill increase by approximately $24 to $36. When you divide that increase across twelve months, it breaks down to just $2 to $3 a month.

What you need to do with your tax statement today

Because this is a one-off tax rebate, you do not need to plan a complex five-year strategy. However, you do need to take immediate practical steps to ensure you are not accidentally overpaying. The first thing you should do is log into the myTax Portal using your Singpass. You need to pull up your 2026 property tax statement and verify that your property is strictly classified under the owner-occupier tax rate.

The Singapore tax system has two entirely different pricing tiers. If the government thinks you are renting out your flat, they will charge you the non-owner-occupier rate. This rate is higher and costs significantly more a year. More importantly, the 15% tax rebate is only for owner-occupied homes. If you recently moved into your flat but forgot to update your official residential address with the authorities, the system might assume you are an investor. Check your status today and file an appeal if the classification is wrong. Once you confirm your status, you can set up a GIRO payment plan to split your discounted bill into twelve smaller, interest-free monthly deductions.

The hidden reality behind the rebate

While the 15% discount is helpful for your 2026 budget, you must recognise the temporary nature of this relief. This rebate is a one-off cushion, not a permanent change to the tax code. The underlying reality is that the AV of your HDB flat has increased. Your flat is now officially assessed at a higher baseline value than it was three years ago.

If the Ministry of Finance decides not to issue another property tax rebate in 2027, you will suddenly feel the full weight of that higher AV. You must plan your future household budgets with the understanding that property taxes may remain elevated in the coming years. You are shielded for now, but the underlying costs of homeownership in Singapore are still trending upward.

The Bottom Line

The 2026 property tax rebate is a demonstration of the government stepping in to protect citizens from market forces. By absorbing the bulk of the AV increase, they have kept the cost of living in an HDB flat predictable.

Do not ignore the digital notification from IRAS this month. Take ten minutes to log in, verify your owner-occupier status, and confirm that the 15% offset has been successfully applied to your account. Automate your payments through GIRO, and you can comfortably manage your property tax obligations for the rest of the year.

All figures and data cited in this article are based on conditions and information available as of March 2026. This data may change as economic conditions and regulatory policies evolve.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.