If you’re purchasing an HDB resale flat, you likely have to consider paying cash over valuation (COV) for the flat.

While the good news is that all signs point towards the property market moderating, with fewer buyers paying COV for their HDB resale flat in 2023, there is still great demand for resale flats. In turn, prices remain high, and buyers need to be wary of paying COV for HDB resale flats.

In this guide, we’ll explain how to calculate COV, how to check HDB COV to determine how much you may need to pay and how to budget for it properly.

Watch Our Video on COV for HDB Resale Flats

What Is COV for HDB Resale Flats?

Cash Over Valuation, or COV for short, is the difference between the sale price of the flat and its actual valuation by HDB. If the resale flat’s valuation is lower than the agreed price, the buyer has to pay COV for their HDB resale flat in cash and upfront. It cannot be paid by grants, CPF or home loans from HDB or the bank.

When buying a resale HDB flat, it is compulsory to submit a request for valuation from HDB. This estimates how much the resale flat is worth by HDB. A resale buyer can only request an HDB valuation after negotiating with the seller on the selling price and paying the option fee.

Typically, HDB valuation is calculated based on the market value of the units in the same area. Only after a seller and buyer agree on a price and the Option to Purchase (OTP) is granted will HDB assign a valuer to the flat to determine its valuation.

And that’s the tricky part about estimating the COV for HDB resale flats.

How to Calculate COV for HDB Resale Flat When Negotiating The Price

| The agreed sale price of the HDB resale flat | $550,000 |

| Actual valuation of the HDB resale flat (by HDB) | $520,000 |

| COV for HDB resale flat to be paid for in cash | $30,000 |

How to calculate COV is simple. In a sense, the COV is the amount the buyer ‘overpays’ for an HDB resale flat. If the agreed sale price is higher than the actual valuation, the difference is the COV value to be paid in cash.

There’s no way around this. HDB cannot conduct the valuation process any earlier. If the COV exceeds what you expected or budgeted for, you may find it hard to cough up the difference in cash.

However, you can do your own due diligence and figure out how to calculate COV. Often, the valuation of an HDB resale flat is based on the prices of past resale transactions. A good way to figure out how to check HDB COV is to search and compare prices of similar properties within the estate.

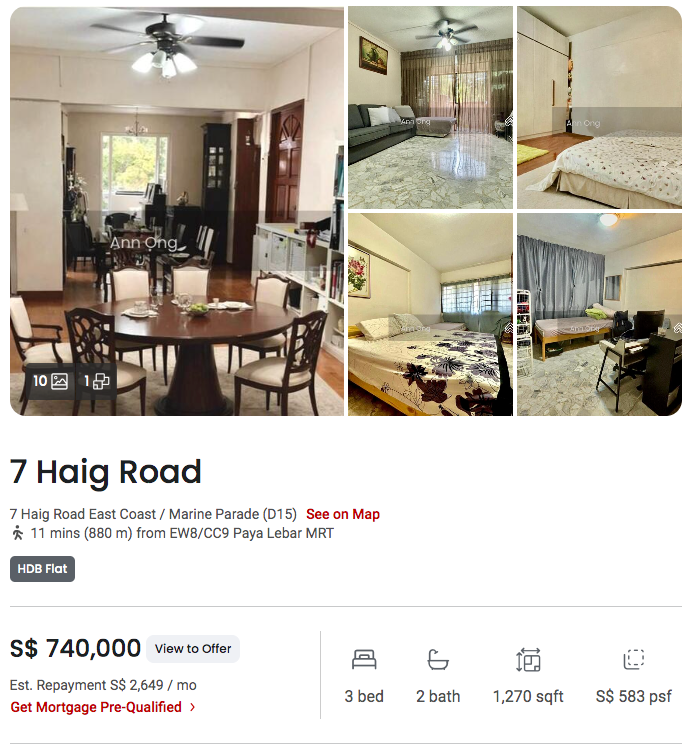

For example, you’re shopping for property on PropertyGuru and eyeing this 5-room flat at 7 Haig Road which has an asking price of $740,000.

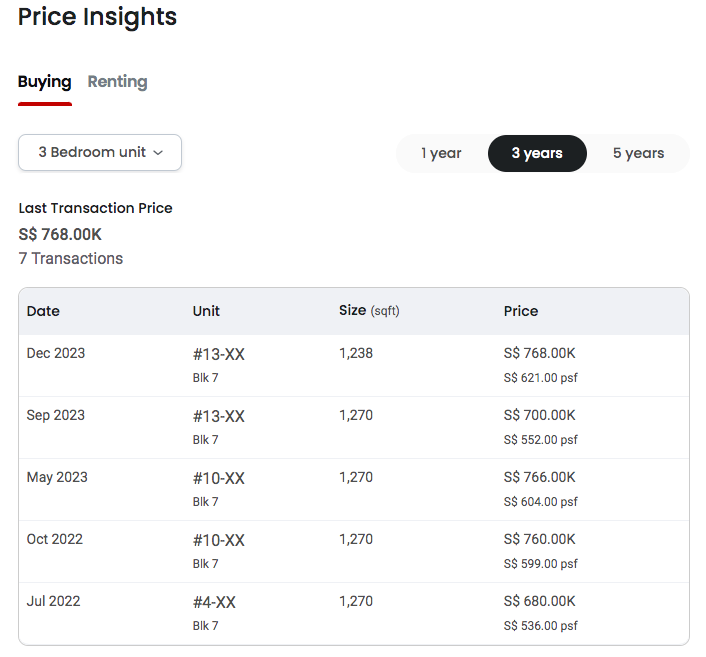

Under each listing, you will find a ‘pricing insights’ section, which pulls up all the data you need, including recent transaction prices and price trends.

Looking at the most recent transactions, you will realise that the two most recent transactions of similar units in the same block were $700,000 in September 2023 and $766,000 in May 2023.

This means the above asking price is likely on par with the current market prices, and you may not have to pay COV if you agree to buy it. But as buyers, we love a good deal. So, you decide to bargain. How low should you go?

The last recorded transaction for such a unit on the HDB Flat Portal was for $750,000 in September 2024.

However, considering that the available pricing for transacted units was on higher floors and the listing you’re looking at is on a low floor, you have some bargaining power. Lower-floor units tend to go for less.

While you can expect the cash over valuation for your HDB resale flat to be around this range, there may be some room to bargain. Hence, you can make an offer with this information in mind.

Other Factors That May Affect An HDB Flat’s Price And/Or Valuation

| Condition | If the flat is well maintained, the COV will likely be higher. If the flat is run down, the COV tends to be lower (if at all). Often, flats with extensive renovations and furnishings come with high COV. |

| Size | If the flat is a larger unit and is no longer being built by HDB, it will likely come with a higher price and maybe COV. |

| Lease | Your price should be based on the remaining years of the lease. A resale buyer won’t get the full 99-year lease, but most flats should have enough for buying a home to stay in. As the remaining lease shortens, the property’s price, value, and usually COV will also decrease. |

| Location | Flats on higher floors and close to key amenities usually command a higher COV. Generally, flats in older estates will be higher in price, as most conveniences have built up over time in the estate. Resale flats located near MRT stations, have many bus routes, and are within reach of the CBD or town area will also typically come with COV. |

| Scarcity | Rare units like executive maisonettes and flats in mature estates like Tiong Bahru command higher prices as HDB is no longer building them. COV may be higher unless the market value is already high due to the scarcity and the asking price has taken this into account. |

Is Paying COV Always a Bad Thing?

Cash over valuation for HDB flats is unique to the buying of resale flats, but there are many reasons why many buyers still go ahead with it.

The more expensive resale flats are often found in mature estates, near the MRT stations, and/or well-serviced by supermarkets, provision shops, hawker centres, shopping malls and choice schools. Moreover, these resale flats are typically more spacious than new BTO flats and are often move-in ready.

As such, many buyers will pay a premium for the above factors. So, if you have the means, paying cash over valuation for an HDB flat might not be a bad thing to secure your dream home.

Depending on the buyer’s urgency to move in, COV can expedite the sale process when the seller accepts a higher transaction price. In short, you can offer a higher price to ‘chope’ your preferred unit.

Browse all HDB Resale Flat sale Listings on PropertyGuru

Ready to find your dream HDB resale flat?

It is important to note that the valuation of the HDB resale flat also affects the amount of Buyer’s Stamp Duty (BSD) to be paid. This is calculated based on the purchase price or market value of the property, whichever is higher (i.e. you will pay more).

Additionally, the Loan-to-Value ratio (LTV) will be applied to the valuation of the resale HDB flat. For example, if you paid $550,000 for a property valued at $520,000, the LTV will apply to the $520,000 valuation and not the full $550,000 you agreed on.

And that’s it! Hopefully, this article has given you a better understanding of how COV works.

For more property news, content and resources, check out PropertyGuru’s guides section.

Looking for a new home? Head to PropertyGuru to browse the top properties for sale in Singapore.

Disclaimer: The information is provided for general information only. PropertyGuru Pte Ltd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.