The Singapore market is very different today from what it was four years ago.

For this edition of the Guru View, we take a look back at the past four years, to see how the real estate market has moved.

By Chang Hui Chew

The past four years have been characterized by cooling measures, an attempt by the Singaporean state to prevent prices from inflating dramatically and becoming a property bubble.

In general, most agree that cooling the markets was a necessary move. When property prices escalate too rapidly, prices often inflate beyond the real value of the home, resulting in families and individuals paying mortgages higher than the worth of their home.

As such, the government introduced a series of measures to curb cycles of speculation and property flipping. These included new regulations that prevented individuals and families from over-leveraging, and made it more expensive for foreigners to enter the market with punitive duties.

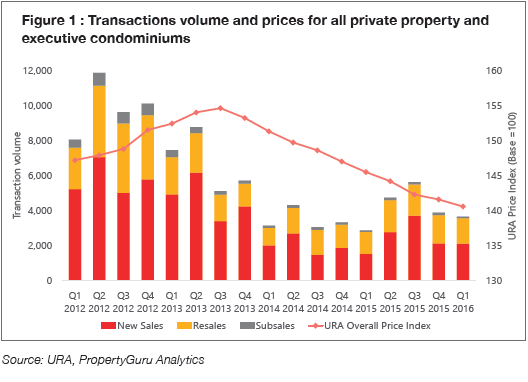

Figure 1 shows the Urban Redevelopment Authority’s overall Private Property Price Index, which takes into account executive condominiums (ECs) as well. With the implementation of cooling measures, prices began to see declines from Q4 2013.

Transaction volumes also tumbled, with sub-sale activity practically drying out, as measures to curb property flipping took their toll. The primary sales market, which made up the majority of transactions per quarter, saw sharp falls as well.

While 2014 was a low point for transaction volumes, with an average of about 2,000 new units sold per quarter, it saw a moderate pick up in 2015. Overall prices however, continued to trend downwards, suggesting that the return of buyers in the market is marked by caution.

For many Singaporeans looking to enter the property market however, this period of price correction was a long time coming, with prices on a steady climb since Q3 2009. This escalation of prices, often perceived to be much faster than the growth in real wages, left many households feeling over-stretched and worried about their finances.

These are the main cooling measures that have led the market to its current state today.

Total Debt Servicing Ratio

Attend any real estate seminar, and the local experts will invariably mention the Total Debt Servicing Ratio (TDSR) as the “mother of all cooling measures”.

Introduced by the Monetary Authority of Singapore (MAS) in June 2013, TDSR limits the amount of a borrower’s monthly income that can be used for debt repayment to 60 percent. This 60 percent is not merely for mortgages, but for all of an individual’s debt, including credit card repayments, car loans and student loans. MAS also changed the way age is used to calculate loan tenures, and implemented a 30 percent haircut to variable incomes.

To round out this set of financially prudent measures, MAS also mandated a stress test of a 3.5 percent interest rate (or the current rate if it is higher). These stress rates are higher than the current prevailing interest rate.

With the implementation of TDSR, many home buyers found themselves unable to muster the funds to purchase new homes. It also curbed the enthusiasm of many investors, who traditionally only needed to put up the downpayment, and then rely on rental incomes to pay off the mortgages.

In 2015’s Financial Stability Review, MAS gave itself a congratulatory pat on the back, emphasizing that over-leveraged households have fallen since the implementation of loan curbs. According to MAS, median households within the three income bands considered (less than $7,000 a month; between $7,001 and $12,000 a month; and, more than $12,000 a month) will still be able to afford their mortgages, even if incomes were to decline by 10 percent, and interest rates were to climb by 300 basis points (bps).

Singaporeans who want to use real estate investments for passive income or to build a nest egg will have to contend with TDSR for the foreseeable future. The government has repeated time and again that TDSR is to prevent households from becoming over-leveraged, and as such, will be a permanent regulation.

Despite the state’s attempt to instill fiduciary prudence through regulation, many investors are still active in the property market. They have, however, turned their sights overseas, diversifying instead into blue chip investment hotspots like Australia and the United Kingdom, or nearby developing markets, like Thailand, Cambodia and Vietnam, that have lower barriers to entry.

While risks are higher overseas, many foreign developers are offering terms that are almost too good to be true, including guaranteed rental returns, deferred payment and buy back schemes. For investors whose affordability has been hit by TDSR and are looking at overseas markets, we cannot emphasize enough the need to consider currency risks, as well as foreign laws and tax structures.

Additional Buyer’s Stamp Duty

For real estate developers and agencies, Additional Buyers Stamp Duty (ABSD) is a particularly punitive measure to their respective businesses. This is especially so for the luxury and higher end segments, which have traditionally relied on foreign buyers to support their sales and cash flows.

Under ABSD, foreigners are required to pay a 15 percent ABSD, no matter if they are first-time buyers or already own multiple Singaporean properties. For a $5 million luxury condo in Singapore’s central region, the ABSD itself would cost the buyer $750,000.

Developers are hit doubly by this particular measure. Not only does this discourage foreigners’ wealth from flowing into their coffers, ABSD regulations also mandate that developers need to sell all their units within five years of purchasing a site, or pay a 10 percent levy. For sites purchased after January 2013, this sum increases to 15 percent.

This particular move on the part of the government is to prevent developers from using their deep pockets and financial power to buy up sites in a down market, and then hoard the launches to when the property cycle swings upwards, to maximize their profits. This also places huge pressures on developers to price their units affordably and move them quickly.

However, PropertyGuru also understands that on the ground, some developers have tried to offer deferred payment schemes, where buyers only pay a small sum upfront, and defer their mortgage payments to after the units are completed. This allows investor-buyers to service their mortgages with rental income instead of taking it out of pocket.

The URA frowns upon such schemes, because it upsets the current system of exercising options to purchase. The timeliness, reliability and validity of URA’s data relies on the assumption that most people exercise their options, and see the entire purchase through.

Such deferred payment schemes would allow developers to mark their units as sold, and prevent it from counting towards their ABSD levy and Qualifying Charges (QC), for foreign or publicly-listed developers, even if buyers walk out of the deal and forfeit their downpayments.

However, since the URA has stepped in and asked developers to cease such schemes, they likely have to find other ways to sell these units. The easiest way of course, would be to slash prices and absorb the losses. Developers however, have staunchly refused to do so for various reasons, and have made repeated calls for the cooling measures, especially ABSD, to be tweaked.

Since the implementation of the cooling measures, several developers, especially those for high-end property, have reported losses of profit and revenues. Some smaller players have also chosen to de-list from the stock exchanges, to prevent paying QC, which could wipe tens of millions of dollars off developers’ profits.

Developers however, see little sympathy from the public in general. In the latest PropertyGuru Sentiment Survey, more than half of the respondents felt that prices of new launches should see some form of price regulation, and more than two-thirds felt that current cooling measures should remain firmly in place.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||