In land-scare Singapore, space is a luxury. A spacious property that can house three generations comfortably is increasingly rare. While many remember the brisk sales and popularity of “mickey mouse” apartments a few years ago, President Halimah’s jumbo HDB flat has brought the spotlight to larger units. So what is the attraction of a larger home?

For starters, a larger residential property will allow the homeowner to age in place; allowing them to go through all stages of life without the hassle of constant moving. On the other hand, the owner of a small unit is likely to have to move several times to cater to his changing housing requirements as his family structure changes.

While a young couple can live quite comfortably in an apartment of 500 square foot (sq ft.), it will hardly be comfortable when the little ones arrive. A larger unit will not only provide individual bedrooms for each child but also give the parents some much needed privacy. When the children get older and move out, their grandparents can move in thus allowing the couple to look after their elderly parents easily.

A larger unit gives the homeowner the option of renting out the extra rooms for additional income when the homeowner retires. The possibility of rental income also acts as a buffer against financial hardship if the homeowner finds himself in need of some additional income.

Source: CapitaLand

Many buyers choose a smaller unit over a larger unit purely because of the lower total price. However, this may prove to be penny wise pound foolish especially when the buyer can well afford the larger unit. The price per square foot (psf) is usually higher for a smaller unit compared to a larger one.

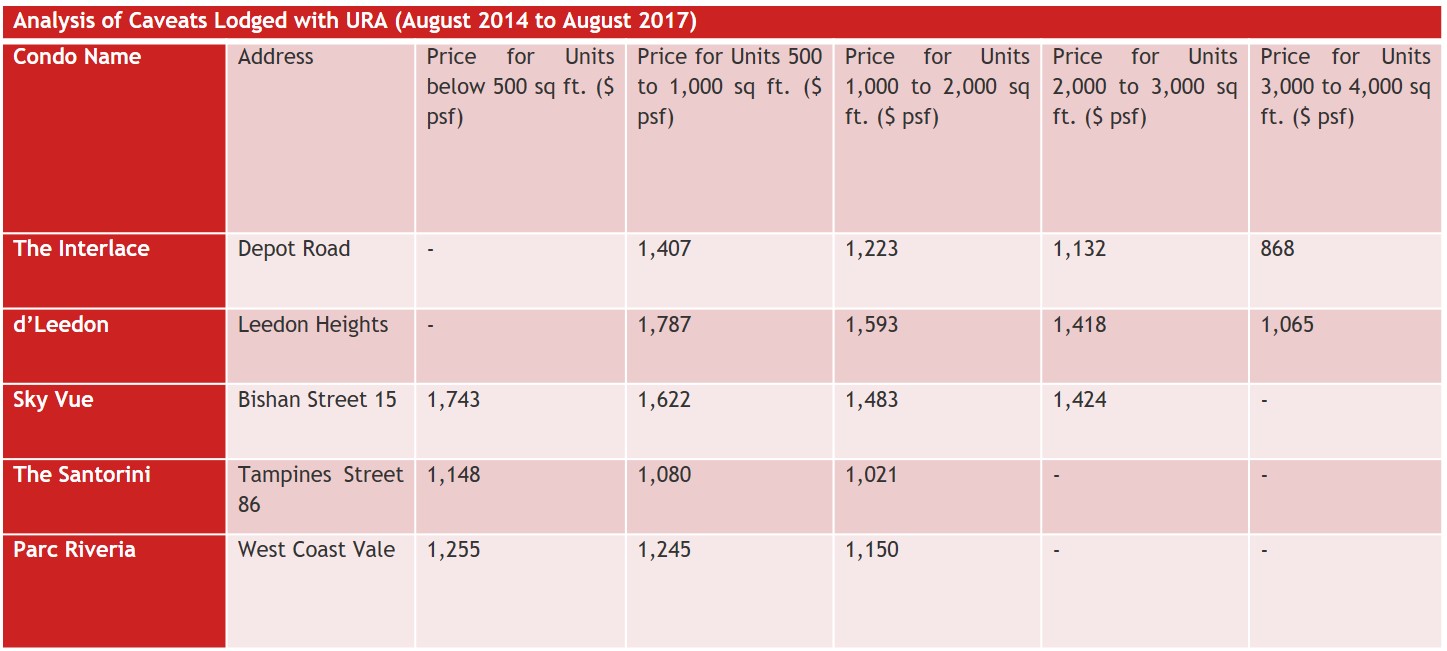

A quick analyst of caveats lodged with the Urban Redevelopment Authority (URA) over the last three years will easily prove this point. Smaller units of 500 to 1,000 sq ft. in The Interlace transacted at an average price of $1,407 psf while larger units of 3,000 to 4,000 sq ft. were sold at a significantly lower $868 psf.

The same can be seen for d’Leedon. Units of 500 to 1,000 sq ft. fetched at an average price of $1,787 psf while units of 3,000 to 4,000 sq ft. transacted at $1,065 psf. These two condominiums are located in the central region of Singapore but an analysis of transactions for mass market condominiums indicates that the trends also holds true for suburban projects.

Smaller units of below 500 sq ft. for Sky Vue, The Santorini and Parc Riveria sold for at least $100 psf higher than larger units of 1,000 to 2,000 sq ft. It is quite clear that a larger unit gives the buyer more bang for his buck.

Source: URA, PropertyGuru

Many investors buy smaller units for investment but the savvy investor should not blindly follow the herd. The lack of space means that only singles or young couples with no children will rent a studio or one-bedroom apartment. However, a two-bedroom unit can comfortably accommodate a family of four. A single or a smaller family who want more space will also look for larger units. As such, a larger unit actually widens the potential tenant pool for the investor.

While the case for a larger unit can easily be made, the argument is less clear-cut for freehold or leasehold properties.

Ask any homebuyer and it is likely that most of them will tell you that they will prefer to buy a freehold property. This is because they think that the freehold tenure allows them to own the property forever unlike a leasehold property which reverts back to the government after the tenure expires. However, freehold does not always mean forever.

In Singapore, land is often compulsory acquired by the government for the construction of infrastructure works such as roads, expressways and MRT rails. In such cases, the homeowners will have no choice but to sell their property to the government. Compulsory acquisition by the government affects both freehold and leasehold properties.

Older freehold properties are also more likely to be put up for en-bloc sales. En-bloc sale of a freehold development tend to fetch better prices for their owners compared to the en-bloc sale of their leasehold counterpart. Developers who purchase such freehold developments do not need to pay a development premium to the government to top up the tenure back to 99-years unlike a leasehold development.

As such, the developer may have more money in the kitty to pay the owners of a freehold development. The development premium can be a hefty sum. Calculation of development premiums is based on development charges. URA just announced that development charges for the six months with effect from 1 September 2017 have been revised upwards. According to URA, development charges for non-land residential land has increased an average of 13.8% compared to the earlier rates.

Freehold properties have an advantage when it comes to financing. Banks generally restrict the duration of the loan if the property being mortgaged has a short remaining tenure. However, this has no impact on newer properties regardless of their tenure. The impact can be truly felt only when the property has less than 60-years of remaining tenure. In Singapore, it is uncommon to find such properties due to an active en-bloc market.

Source: CapitaLand

However, it is not all roses for freehold properties. For a buyer who is purchasing the property to rent out, it will make more financial sense to invest in a leasehold property. For starters, a leasehold property is generally less expensive than a comparable freehold property which means less initial capital outlay for a leasehold property. Secondly, leasehold properties can potentially generate a higher rental yield.

Tenants are not concerned about the tenure of their rental property. They are more concerned about its location and surrounding amenities. So a well-located leasehold property with many nearby amenities is likely to fetch a higher rent than a freehold property in a less desirable location. Even if both properties are in the same location, the leasehold property will still give the investor a higher rental yield because of the lower capital outlay.

So does it make more sense to buy a freehold or a leasehold property? That will depend greatly on the intentions of the buyer. If the buyer plans to live in the property with his family for the long term, then a freehold property is the way to go. However, if the buyer is purchasing an investment property for rental income, then the leasehold property may be a wiser choice.

For more information about our Living Large Specials, go to: livinglarge.propertyguru.com.sg