Property developers certainly did not have the easiest year in 2014, with the various rounds of cooling measures still possessing strong influence over buyers’ appetite. Bearing testament of the cooling market is the consecutive quarter-on-quarter decline in non-landed private residential property prices, the fifth so far as of the final quarter of 2014, a further sign that the nation’s once red hot property market has significantly cooled.

Subdued price performance the norm

In overall, transactions across the regions have fallen. So far, the chill in the sales market appears to be concentrated mainly in the upmarket condo segment. The CCR region suffered the greatest drop with only a total of 1054 units sold in 2014 – over 3 times lesser as compared to 2013. Looking into the mass market segment in the OCR, transactions have also dipped 156 percent year-on-year to 5903 units.

This sharp decline is an indication that suburban homes, perennially thought to be more popular option due to their cheaper price quantum, could be at risk. Before the TDSR was imposed, mass-market home sales made up the bulk of the volume, forming an average of 60 percent of total sales. This dominance has since waned, with the OCR constituting 49 percent of sales in 2014.

As for the mid-tier housing in the RCR, it appears to be the most resilient with 4,596 units sold, a smaller drop of 43 percent from 2013 figures. The relatively stable trend noticed in the RCR corresponds to the rise in a number of appropriately priced apartments, such as the recently launched Highline Residences and City Gate which appeal to cash-strapped buyers.

On the back of declining transactions, a reduction in prices is a clear consequence of the government’s recent cooling measure taking effect. Condos in the CCR saw a drop in prices of 0.9 percent in Q4, higher than the 0.8 percent drop in the quarter prior. Within the same quarter, prices in the RCR and OCR both registered worse results with prices sliding 1.2 percent and 0.9 percent respectively compared to their respective decreases of 0.4 percent and 0.3 percent in Q3. For the whole of 2014, prices in CCR, RCR and OCR have fallen individually by 4.1 percent, 5.2 percent and 2.2 percent.

Current behaviour likely to persist

By now, the most pressing question on the minds of property observers is for how much further the market will correct by. Indeed, to those who have invested in the condo market, regardless of whether they are current owners of a single private property or those who have bought multiple ones, the last 15 months were a turbulent period. Unfortunately, barring external shocks, analysts have predicted that there is a high probability that the property malaise is here to stay for the majority of 2015.

New launch prices: The lower, the better

In view of the prevailing market conditions, property developers have come to the realisation that necessary price adjustments on their new launches have to be made. As with what had occurred in 2014, it would not be meaningful to price new units based on what developers think is profitable, but more on what is affordable to buyers within a specific locality that will drive sales.

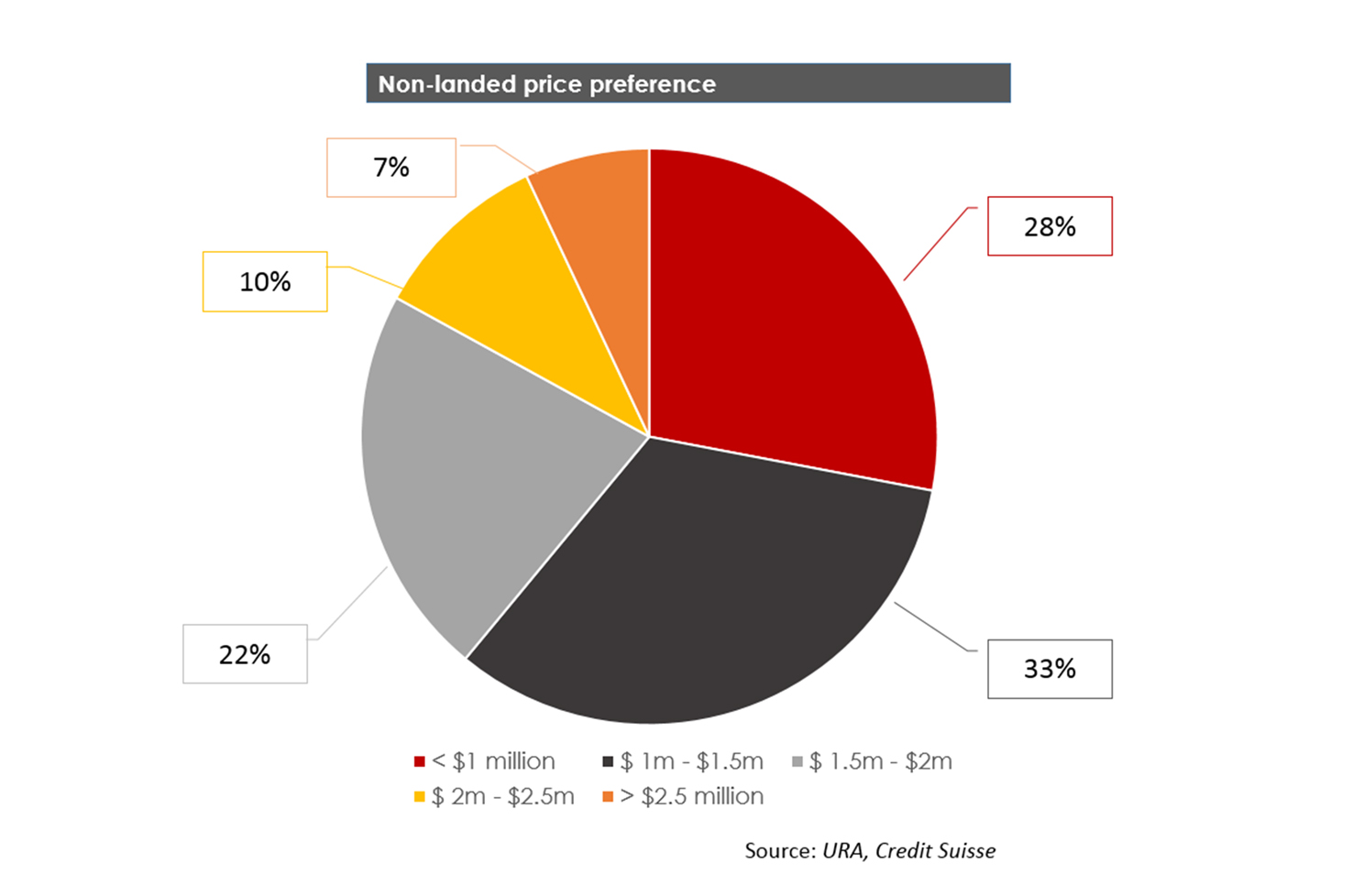

“For developers, they may gradually adjust their prices so that their projects are more affordable to a bigger pool of buyers. For mid-sized mass market private homes of 800 – 1100 sq in size, the sweet spot price range will typically be between $900,000 and $1.1 million. Projects beyond $1.2 million might be a stretch for most middle and upper middle income buyers,” mentioned Alice Tan, Director& Head of Consultancy and Research at Knight Frank.

Further elaborating on how pricing affects demand, she added, “City fringe homes should ideally be priced between $1.2 – $1.5 million for a 2 or 3 bedroom unit. Any project which surpasses the $2 million mark will be less attractive to prospective buyers because they would be unable to fulfil their TDSR limitations.”

Preference for smaller units

Indeed, with severely constrained borrowing under the TDSR, there are probably much fewer potential buyers who are interested in purchasing a condo. And if they are still in the market, their budgets would have been substantially cut. As a result, buyers’ preferences are changing, opting to move towards smaller living spaces which cater to both their immediate housing needs as well as financial situation.

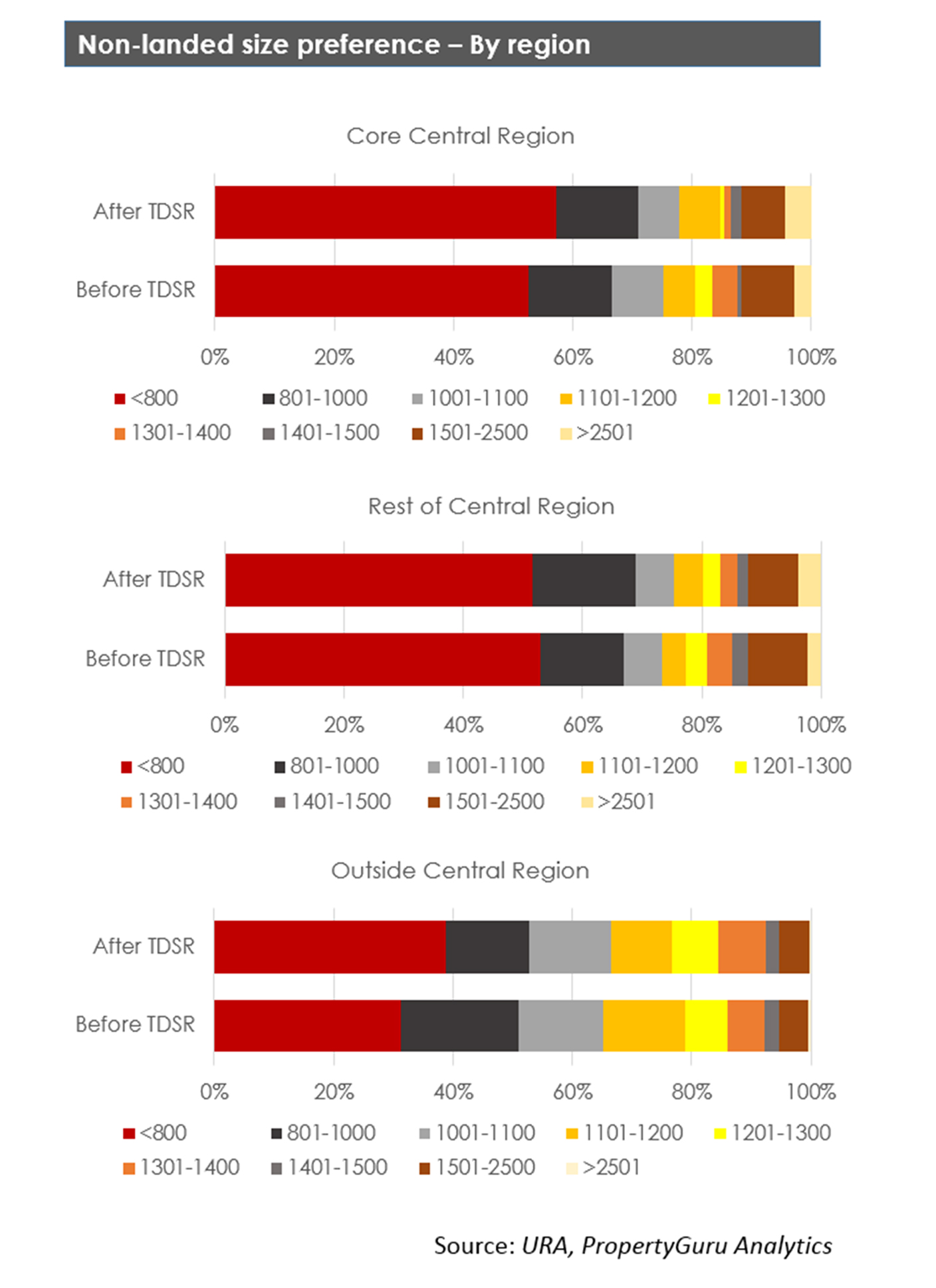

Looking at both new sales and resale transactions in 2014 alone, 30 percent of units sold are 800 sq ft and below – the average size of a 1 or 2 bedroom unit. In fact, upon closer inspection of preferred size of property pre and post TDSR, it can be said that property seekers have been gravitating towards smaller units in each of the regions.

In the OCR and CCR, there has been a marked increase from 14 to 17 percent and from 53 to 57 percent respectively for condos 800 sq ft and less. On the other hand, those buying into the RCR tend to focus more into apartments sized in the range of 801 to 1000 sq ft, showing a rise from 14 to 17 percent as well.

The effect of TDSR on home sizes was even more pronounced within the new sales market. The median floor area of new homes bought from developers between Q3 2013 (when the TDSR was introduced) and Q4 2014 was at 753 sq ft, 12.5 per cent smaller than the median size of 861 sq ft in the first six months of 2013 before TDSR was imposed.

Remaining on the path of moderation in 2015

Most property analysts are in agreement that a further price correction is inevitable in 2015, together with a similar fall in transaction figures. It is a common consensus that so long as prevailing factors in the market do not change – namely from continued enforcement of cooling measures to enforce a tighter credit environment and an anticipation of a large supply of new homes – the private residential property market will remain bearish.

While acknowledging that further moderation of prices and transactions are foreseeable, 2015’s pace of decline is not projected to fall at a faster rate in lieu of the provision of stability the cooling measures were designed for. As explained by Eugene Lim, Key Executive Officer at ERA Realty, “Going forward in 2015, the market scenario will be quite similar to 2014, we should expect to see 8000 to 9000 units transacted for the year. Because of this, we can also expect prices to trend downwards in the region of 5 to 8 percent for the whole year.”

Despite the fact that 2015 is slated to mirror the trends set in 2014, there is optimism that buying activity may pick up towards the end of the year. This is due to the belief that prices would have bottomed out sufficiently by Q2/Q3, encouraging buyers to seize the opportunity and re-enter the market.

“As the cooling measures do not look like they will be eased in the short term, property sellers will be more realistic in 2015. Coupled with falling rents, this will encourage more instances of pressured selling as current property owners may not be able to cover their mortgage payments. As a result, there might be more flexibility, in terms of pricing, by sellers. With that, buyers may be attracted to these lowered prices, encouraging overall volume to go up slightly,” mentioned Ong Teck Hui, National Director – Research for Jones Lang Lasalle.

To read more about the property outlook for 2015, download the PropertyGuru Property Outlook Report 2015 eBook here

Adam Rahman, Senior Content Marketing Executive at PropertyGuru, edited this story. To contact him about this or other stories, email adam@propertyguru.com.sg